Now that we have an understanding of the supply and demand model, we can take a wider view of how resources are allocated within a society.

Due to the economic problem of scarcity, a society must make decisions on which goods and services to produce, how to produce them, and where to distribute them.

In a free market economy, market forces are left to govern production and allocation of resources, without state intervention. In a centrally planned economy, the state plans and directs the production and allocation of resources. A mixed economy contains aspects of both of these types of economy.

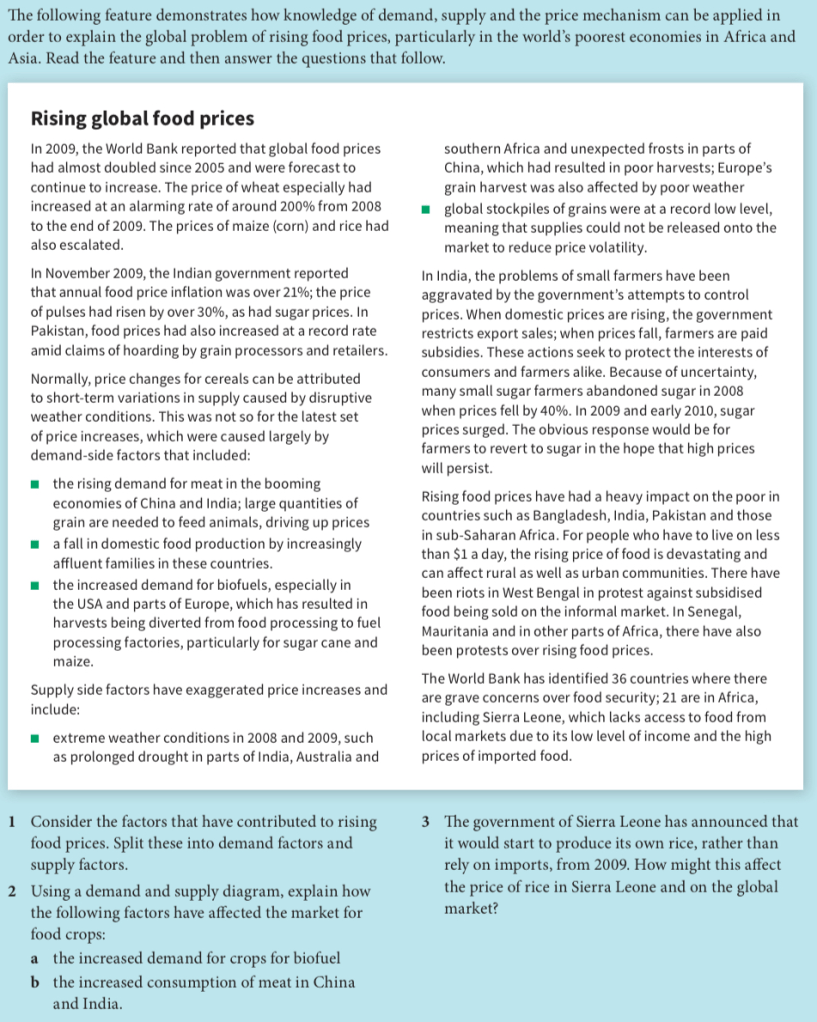

The price of a good serves as an indicator of consumers’ preference within a market. One way we can think of this is to consider the marginal consumer. This consumer would choose not to buy if the price were even slightly above the equilibrium price P*. If we think about society as a whole, P* can be considered as the marginal social benefit (MSB) from consuming the good.

The marginal social benefit is defined as the additional benefit that society gains from consuming an extra unit of a good.

The demand curve represents the price that each consumer is willing to pay for a product. So if we consider the diagram below, consumer A is getting a good deal as he is paying less that he would willingly pay to get the product:

If we consider all these “surplus values”, where consumers are getting benefits that they would have paid more for, the combined amount is known as the consumer surplus, represented by the shaded triangle below:

Task 1

- Identify the area that represents consumer surplus if the price of the good is E;

- If the price then increases to B, which area represents the consumer surplus at this new price?;

- Which area represents the change in consumer surplus between the two positions?

Task 2 – Producer & Consumer Surplus and Elasticity

Explain with the aid of a diagram (one for each question) the impact on consumer and producer surplus in relation to a particular product of:

- Demand for the product becoming more price elastic;

- Supply of the product becoming more price elastic;

- Demand curve for the product shifting to the right, supply remaining unchanged;

- Supply curve shifting to the right; demand remaining unchanged.

Prices as signals

A drop in demand leads to a lower price, which is a signal to producers to supply less, just as an increase in demand leads to a higher price signalling that firms should produce more. Below’s diagram shows how this signalling happened as DVDs were introduced into the market and the demand for videos dropped:

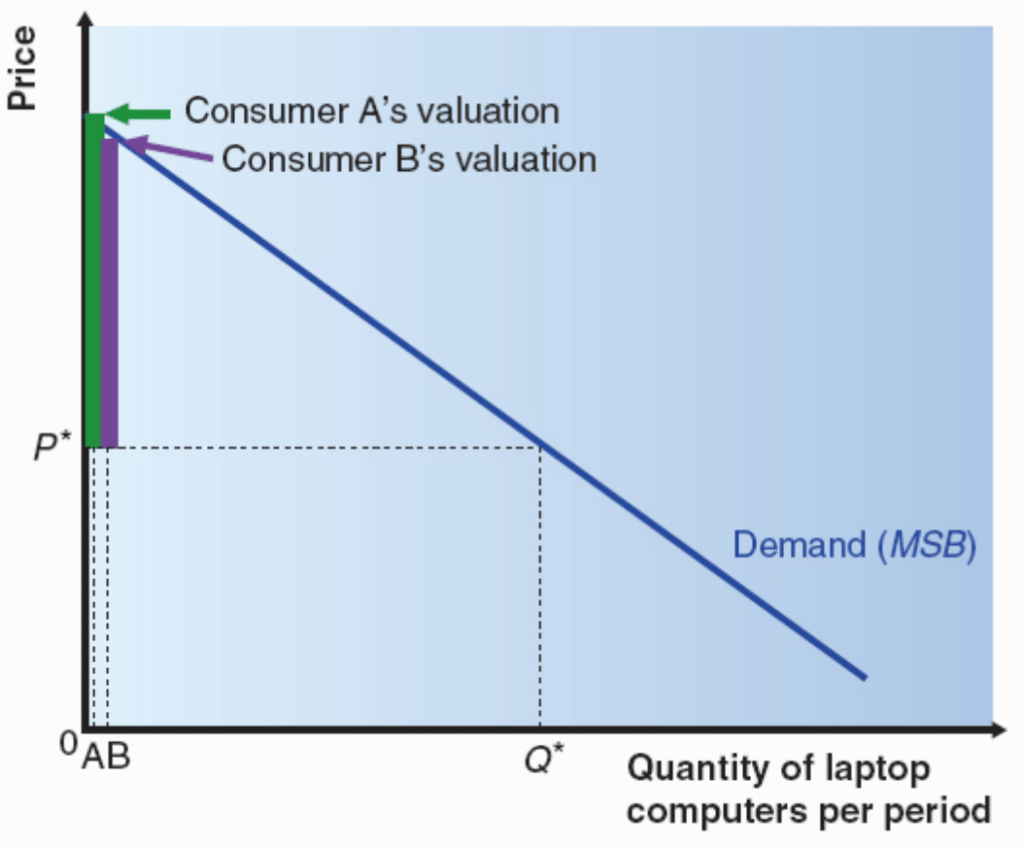

Producer surplus

Producer surplus is the difference between the price received by firms for a good or service and the price at which they would have been prepared to supply that good or service. As with demand, with supply we can consider the supply curve as indicating marginal cost, the cost of producing an additional unit of output.

New firms entering the market

We have so far mostly considered changes due to the consumer, but if an industry seems profitable, naturally new firms will be inclined to join a market, particularly if there are few barriers to entry. This is an example of an increase in demand leading to a subsequent increase in supply. This is shown below (as well as its converse, shown below that):

Task

- Sketch a demand and supply diagram and mark on it the areas that represent consumer and producer surplus;

- Using a demand and supply diagram, explain the process that provides incentives for firms to adjust to a decrease in the demand for fountain pens in a competitive market;

- Think about how you could use demand and supply analysis to explain recent movements in the world price of oil.

Task – Distinguishing supply and demand and considering how they interact