The balance of payments is a set of accounts showing the transactions conducted between residents of a country and the rest of the world. The IMF outlines a standard manner in which to present these accounts.

The accounts include a current account, a capital account and a financial account. Transactions in reserve assets (those held by a country’s central bank to make up for shortfalls in the other accounts) are also identified, as well as a balancing item account for any unidentified errors.

- Balance of Payments

- Current Account

- Trade in Goods (export & import, e.g. cars, TVs). Will be in surplus if export revenue exceeds import expenditure – also known as the visible balance;

- Trade in Services (e.g. tourism, finance) – also known as the invisible balance;

- Income (profits, interest and dividends earned on investment abroad minus foreign earnings on domestic investment) (also called PRIMARY INCOME);

- Current transfers (with no related goods / services, e.g. foreign aid and transfers by private individuals, inc. to relatives) (also called SECONDARY INCOME).

- Capital Account – A small part of the balance of payments, includes things like money brought into and taken out of the country by migrants that have recently become residents and sale and purchase of copyrights, patents and trademarks (i.e. neither goods/services nor financial products).

- Financial Account

- Direct Investment. e.g. Building of a factory or takeover of company, either by domestic firm in foreign country or foreign firm in domestic country.

- Portfolio Investment. e.g. Purchases and sale of government bonds;

- Other investments. e.g. bank loans and inter-governmental loans;

- Reserve assets. Government’s holdings of gold and FX (FX reserves are held to settle international debts and influence the FX rate)

- Balancing Items (i.e. net errors) (can be due to timing issues or lack of information)

- Current Account

Individual Activity

Group Activity – Balance of Payments

In small groups you need to create a presentation titled “Balance of Payments in Georgia during the 21st Century”

The presentation must include the following:

- Explanation of how Georgia presents its balance of payments accounts;

- Identify the current surplus or deficit in the trade in goods and services section of the current account;

- Detail movements in this section of the current account during this period and explain any major shifts;

- Give some explanation of how this surplus or deficit impacts Georgia’s economy.

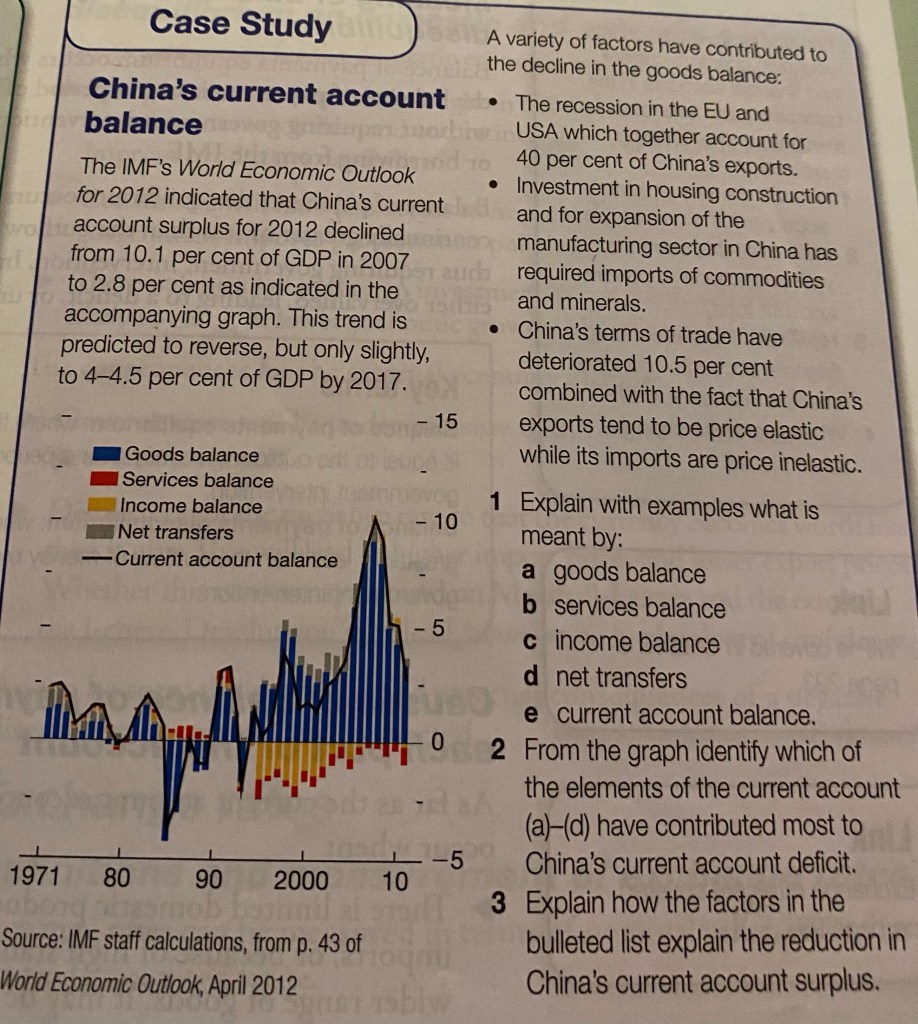

Causes of Current Account Deficit

A current account deficit can be caused by:

- Growing domestic economy (leads to greater purchase of raw materials and capital goods from abroad in the short term) – unlikely to be seen as a problem;

- Declining economic activity with trading partners (recessions in foreign country could affect exports) – known as a cyclical deficit – typically short term and self-correcting;

- Structural problems (lack of competitiveness of domestic firms on the international market. Could be due to overvalued exchange rate, high inflation rate, or low labour and capital productivity) – This is a cause for concern as it may be long-term and not self-correcting.

A current account deficit allows a country’s residents to consume more than the country produces – sometimes referred to as a country living beyond its means. A current account surplus may seem beneficial, but may mean that the country’s residents are not enjoying as high a standard of living as possible. It is often most meaningful to consider the deficit or surplus as a percentage of the country’s GDP. e.g. in 2013 the US had a $400b current account deficit and South Africa’s was $22b. However, as South Africa’s comprised 6.5% of the country’s GDP it was considered more of a cause for concern than the US’s, which comprised only 2.5%.

A financial account deficit is not necessarily a problem, as it can lead to a future cash inflow of profits, interests and dividends. It may be a cause for concern, however, if it results from a long-term lack of confidence in a country’s economic prospects (i.e. capital flight) – this may lead to a recession.

Task 1 – Balance of Payments

Task 2 – Balance of Payments

Task 3 – Balance of Payments

Exchange Rate

The (nominal) exchange rate is the price of one currency in terms of another. The demand for currency is a derived demand, because people want it in order to buy a certain country’s goods, services or assets.

The demand for a country’s goods depends on the relative prices of domestic goods, income, preferences for foreign and domestic goods, and the exchange rate.

Below is the USD:GBP exchange rate from the 1950s to the 2000s. Up until 1967 GBP was pegged to USD at $2.80:£1, this was then devalued to $2.40:£1 and then later was left to float with the market. By 2000 it was at $1.50:£1. Ceteris paribus, this made UK products more competitive in the US as they became more cheaply available.

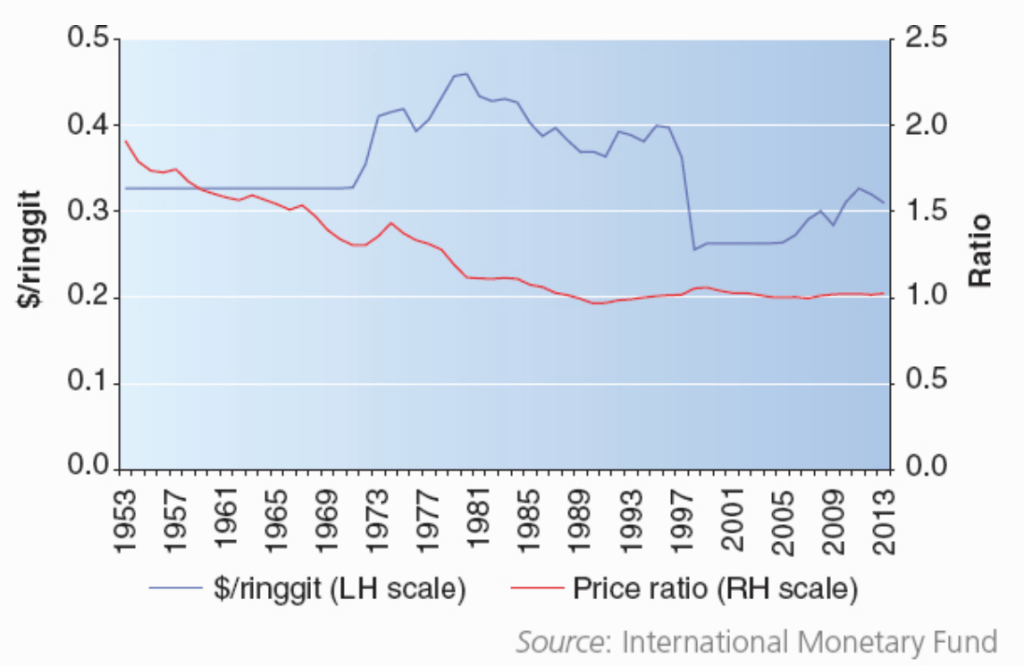

Ceteris paribus is of course not typically accurate, as it doesn’t account for movements in the price of goods. In Malaysia, where the the prices of domestic goods rose more rapidly than in the US, we can see the difference between the (nominal) exchange rate and the ratio fo consumer prices relative to the US, which shows that the two countries experienced inflation at a similar rate from the 1980s onwards.:

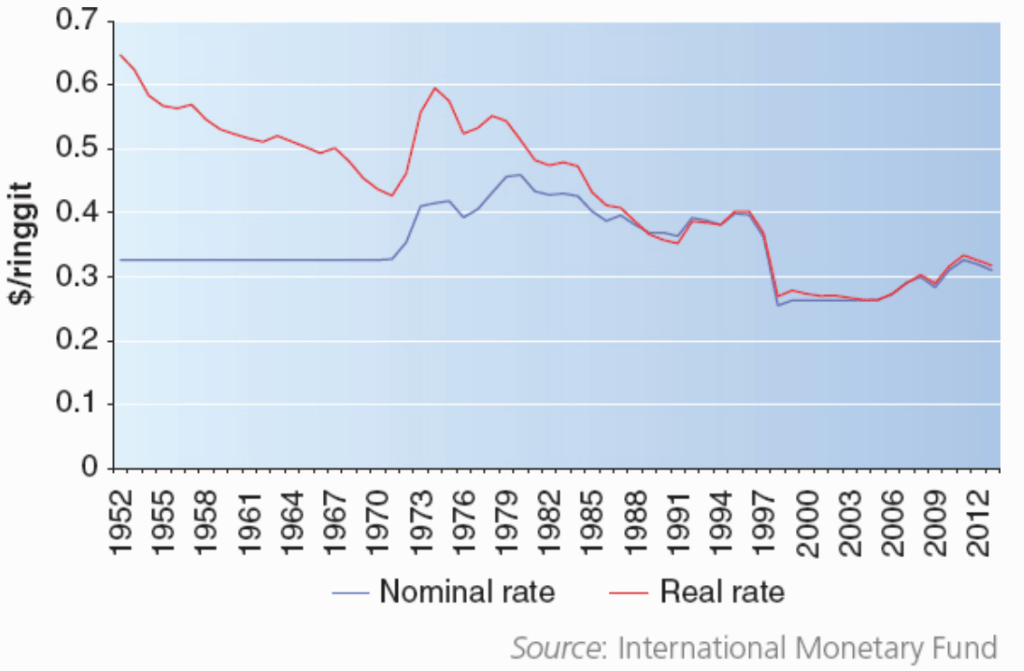

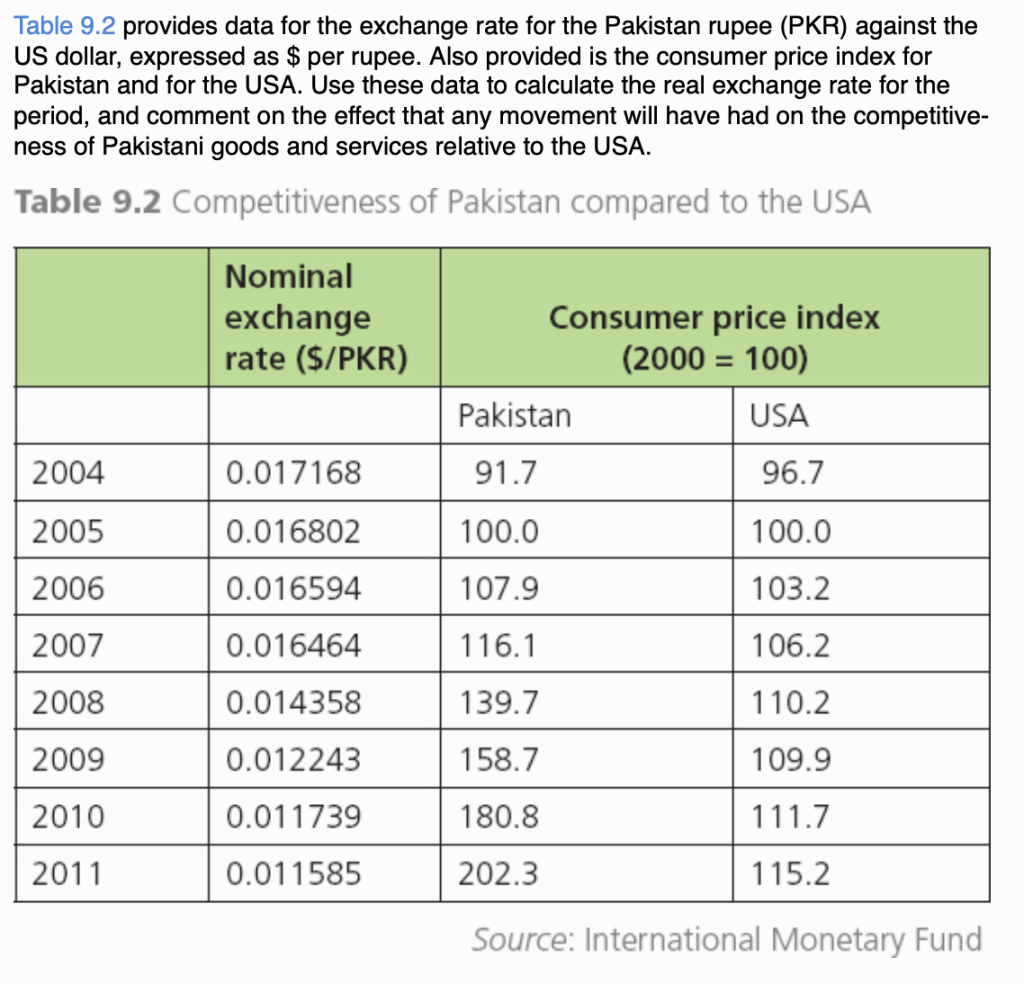

We can calculate a real exchange rate by multiplying the nominal exchange rate by the ratio of relative prices:

As an alternative to measuring two currencies against each other, a country’s currency can be measured against the effective exchange rate (or trade weighted exchange rate), which is a weighted average of exchange rates of the country’s trading partners.

Exercise

The exchange rate and the financial account

International transactions in financial assets also influence, and are influenced by, the exchange rate. High interest rates in the UK can attract an inflow of funds into the UK, helping to fund a current account deficit and putting upward pressure on the exchange rate (in turn affecting the international competitiveness of UK goods and services). So there is a link between movements in the exchange rate and the level of aggregate demand in the economy.

Determining Exchange Rates

Treating the foreign exchange market as a variant of the demand and supply model and leaving the market to find its way to equilibrium is called the floating exchange rate system, however governments may choose not to leave the exchange rate to the market and choose a managed floating exchange rate system, under which the exchange rate is permitted to find its own level in the market within certain limits which prompt government intervention, or a fixed exchange rate system, in which the government commits to maintaining the exchange rate at a specific level against another currency.

The Bretton Woods conference after WWII established a fixed exchange rate system pegged to the dollar, also known as the dollar standard, which remained in place until the early 1970s. In this situation, the country’s central bank buys or sells foreign exchange reserves (stocks of foreign exchange or gold held) to move the exchange rate from its equilibrium point to the fixed rate.

Naturally, a country holding its currency away from equilibrium indefinitely (if the equilibrium is not floating around the pegged rate) will cause problems in the long run. In the early years of the twentieth century China had their currency pegged against the US dollar at such a low level that they were accumulating substantial amounts of US government stock. This kept China’s exports highly competitive in world markets, but relied on their ability to continue to expand domestic production to meet the high demand and avoid deflation.

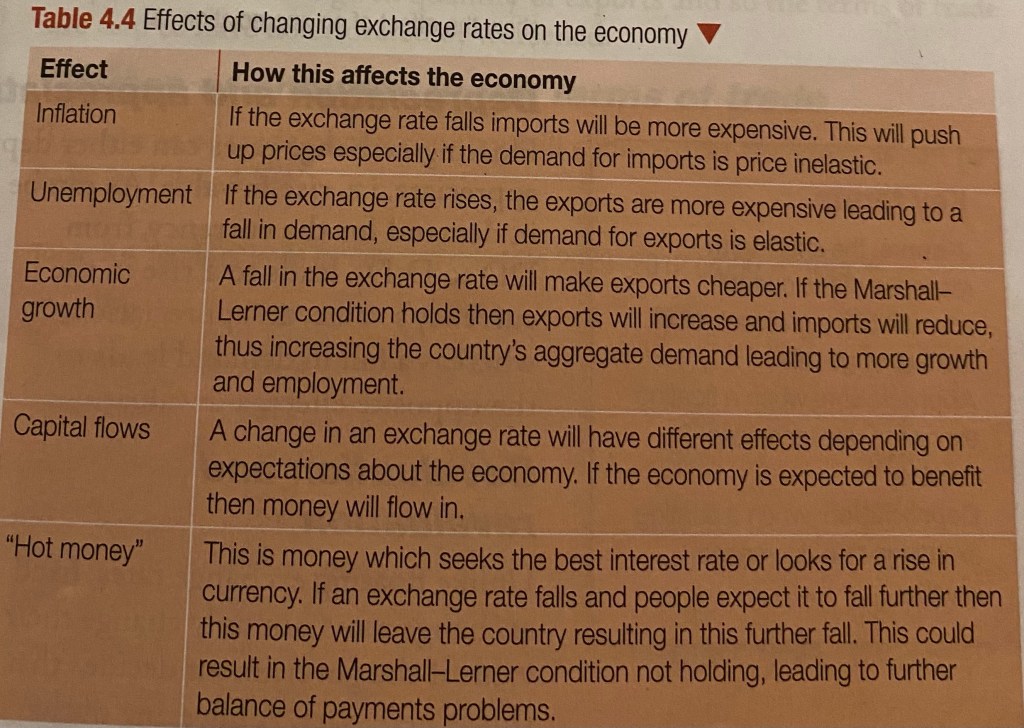

Effects of devaluation

Devaluation, the reduction of the price of a country’s currency relative to an agreed rate, improves competitiveness by shifting the AD curve to the right.

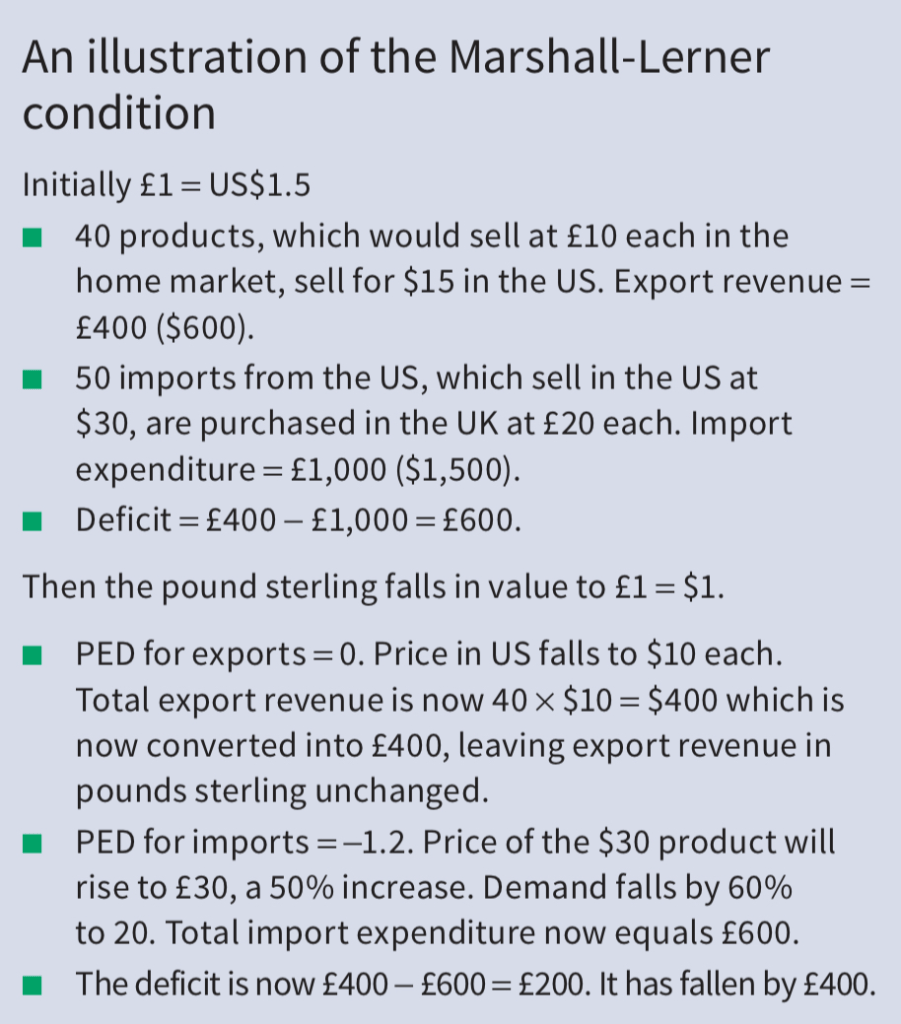

In order for a fall in the exchange rate to cause an improvement in the current account position, it is necessary that the sum of the price elasticities of demand for exports and imports is greater than 1, which is called the Marshall-Lerner condition. Below is a numerical demonstration of the Marshall-Lerner condition:

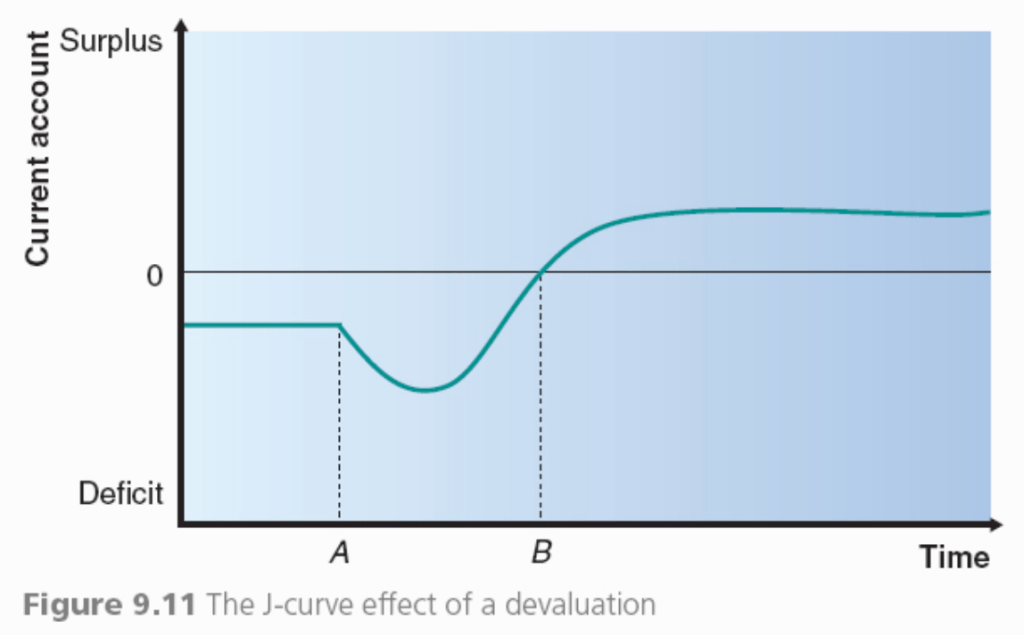

Devaluation doesn’t always lead to an improvement in the current account though. Domestic producers may not have spare capacity, at least in the short term, reducing the impact on exports. This can lead to a J-curve effect, where the current account gets worse in the short term. The graph below shows this scenario with a deflation at time A, and a lag until time B when domestic firms have had time to expand their output:

Part of the reason for the Bretton Woods dollar standard breaking down in the early 1970s was that a peg system relies on the stability of the base currency, and during the 1960s for the US to finance the Vietnam War the supply of dollars began to expand, which led to inflation in countries pegged to the USD making it harder for them to sustain the exchange rates at the fixed level.

Exercise

Floating Exchange Rates

Any increase in the exchange rate within a floating system is called an appreciation, whereas any decrease is called a depreciation. The purchasing power parity theory of exchange rates states that in the long run the exchange rate will adjust to offset any differences in inflation rates between countries. Significant divergence can occur in the short run however, this can cause and also be heavily influenced by speculation (funds known as hot money moving to countries where they can achieve the best return, typically based on the interest rate). Speculation was a key factor in the Asian financial crisis of 1997 as significant flows of capital were moved to Thailand seeking high returns with the subsequent outward flows then putting pressure on the exchange rate, eventually forcing it to devalue.

What are the advantages and disadvantages of a floating exchange rate system?

- Advantages

- Rate should adapt to restore a balance on the current account of the balance of payments;

- Government doesn’t need to hold FX reserves to influence exchange rate and can use these for other purposes & focus on other priorities;

- Disadvantages

- Significant fluctuations can make it difficult to estimate income from selling exports and cost of imports, which can discourage trade (although forward markets can help with this);

- Removes pressure on government to maintain price stability (as they can rely on the FX rate to correct for this – but this can lead to inflationary pressure).

Task – Fixed and Floating Exchange Rates

Hybrid Models (managed floats)

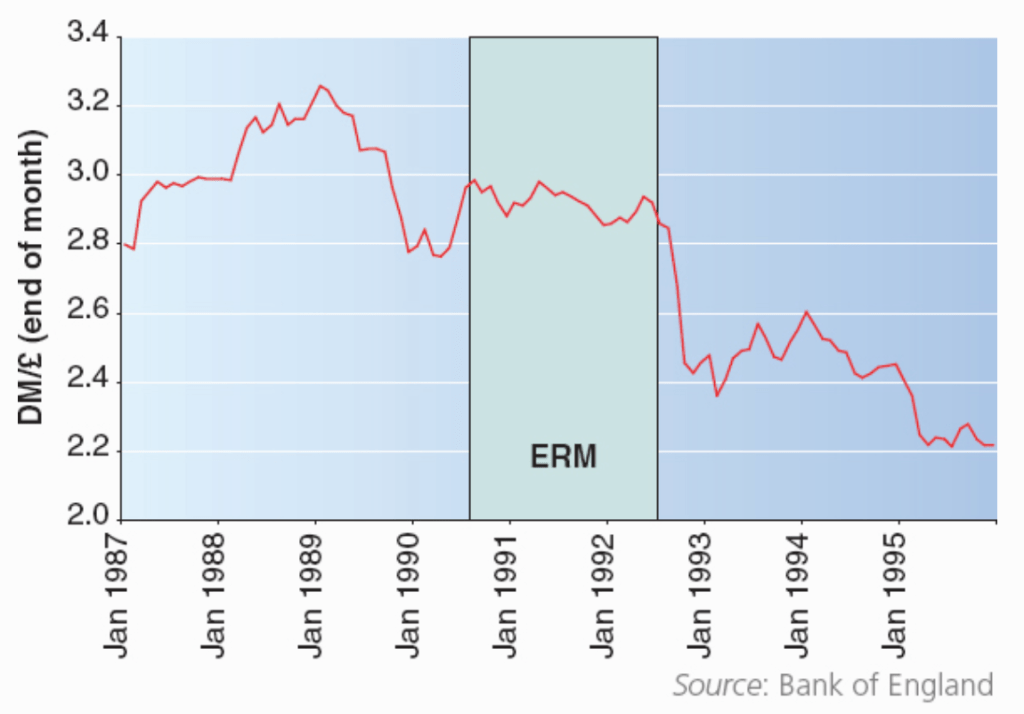

In 1979 the Exchange Rate Mechanism (ERM) was agreed upon by various European countries to avoid excessive divergence of their currencies (by more that 2.25% of the weighted average of the members’ currencies), as part of the European Monetary System (EMS). It was an adjustable peg system, with eleven realignments being permitted between 1979 and 1987.

The UK initially didn’t join the ERM but followed internal policies to keep the rate of the deutschmark at around DM3:£1. They joined in September 1990 with an agreed 6% fluctuation limit, however the rate set against the deutschmark was high, a situation worsened by the effects of German reunification which led to substantial capital flows into Germany. Hence, following significant speculative attacks depleting the Bank of England’s foreign exchange reserves, Britain left the ERM in 1992. The graph below tracks this period:

Task – China’s Exchange Rate System

Balance of payments problems

In a fixed exchange rate regime, there is a limit to how long a country can hold their exchange rate away from equilibrium, as foreign exchange reserves are limited. In a floating exchange rate regime, if the current account is in deficit, then the earnings from exports are not sufficient to pay for imports. If this is sustained, then the financial account requires a sustained surplus, which means the country is effectively exporting assets. If these become less attractive to foreign investors they will need to raise interest rates, leading to a leakage of investment income in the future.

A fundamental cause of a deficit on the current account is a lack of competitiveness of domestic goods and services, either from an overvalued exchange rate or from high relative prices of domestic goods and services. This may indicate a need to improve the efficiency of production, or reduce domestic incomes.

Task – Current Account Deficit