Introductory Task

The way firms behave is strongly influenced by the market environment that they exist in. We will look at the structure of different markets, in particular the number of firms operating in them:

Perfect competition is the extreme situation where each firm in the market is a price taker. It occurs if the products produced are indistinguishable and firms are relatively free to enter or exit the market. The market price will be pushed down to that where a typical firm just makes enough profit to stay in business. Any supernormal profits will attract other firms into the market, removing the profit. Any firms not making sufficient profit will leave the market, allowing the price to increase to the point where firms make enough profit to stay in business.

A monopoly is the opposite extreme, with only one firm in operation. This firm can influence price and can choose their desired combination of price and output to maximise profits. In choosing price however, they are subject to the demand curve, and can only choose points on this curve. The firm in a monopoly produces a product with no close substitutes, like spaceships. Due to barriers to entry to the market, the firm can increase prices and make supernormal profits without attracting new competitors.

Between these two extremes are monopolistic competition and oligopoly. In monopolistic competition there are many, typically relatively small, firms, each producing similar but not identical products, and with some scope for influencing price, for instance due to brand loyalty. Local bakeries would be an example of monopolistic competition. An oligopoly is a market with just a few firms in which the decisions of each firm heavily impact the others. Such situation incentivises collusion in cartels, in order to behave as a monopoly.

Perfect competition

Perfect competition is a form of market structure that produces allocative and productive efficiency in long-run equilibrium. This model is kind of a theoretic ideal, which gives a benchmark by which other market structures can be analysed. It relies on the following assumptions:

- Firms aim to maximise profits;

- Market has many participants (buyers and sellers);

- Product is homogeneous;

- The market has no barriers to entry or exit;

- Participants have perfect knowledge of market conditions.

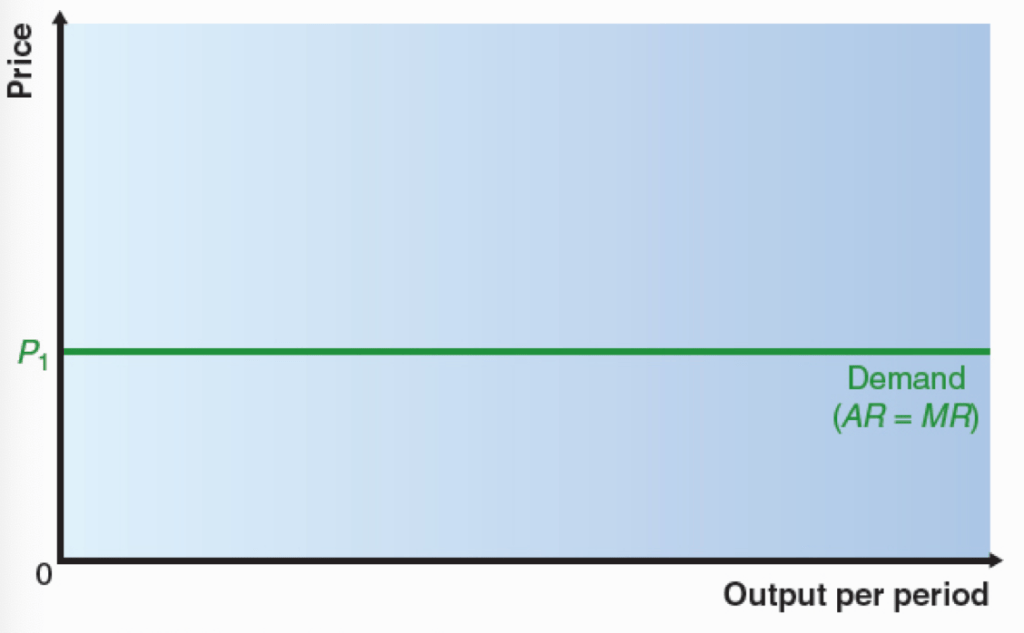

Under the following assumptions, we can analyse how a firm will operate in a market. In these conditions an individual cannot influence the price, i.e. they are a price taker and face a perfectly elastic demand curve for their product, as shown below. If they raise their price, they will sell nothing, and they have no incentive to decrease their price as there are no limits to the amount they can sell at the equilibrium price.

Task – Price in Perfectly Competitive Market

Given the characteristics of a perfectly competitive market, explain why an individual firm would not reduce its price in a perfectly competitive market.

Production amount

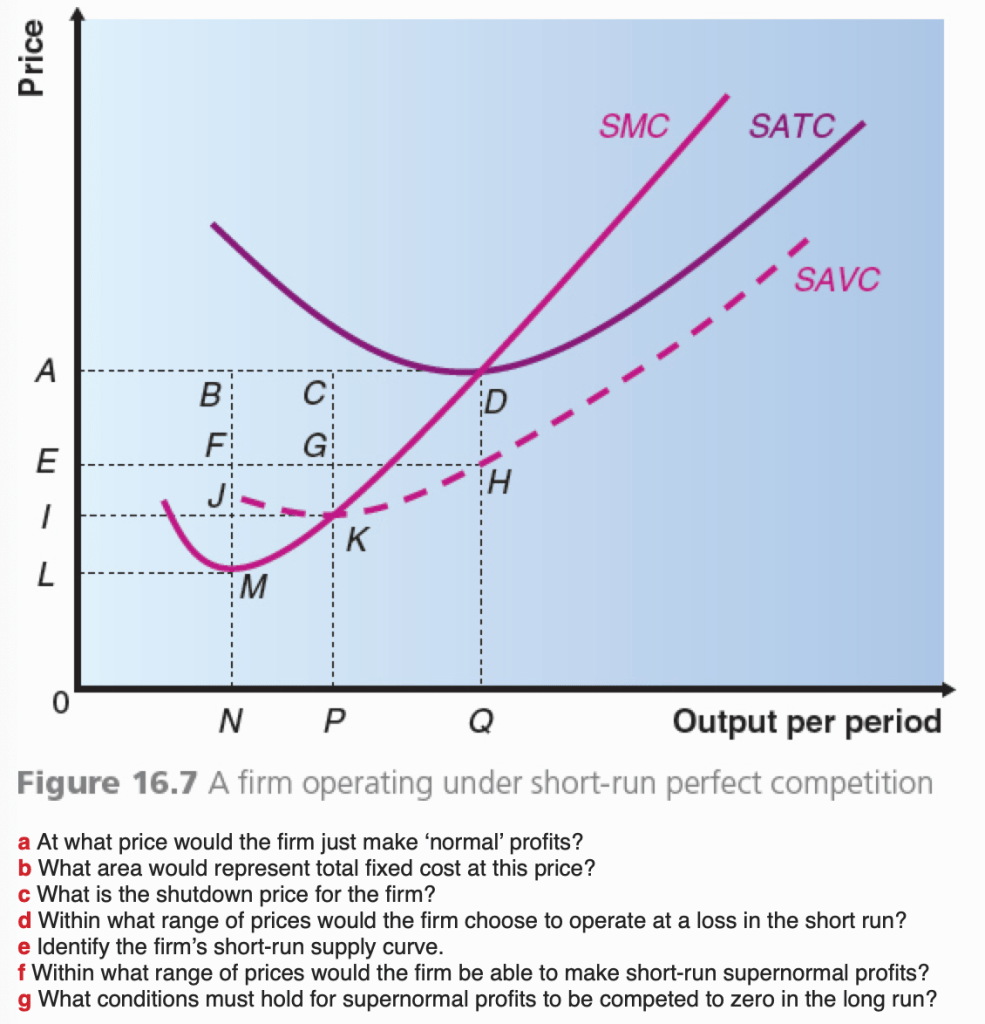

How much will they choose to sell? In order to maximise profits, they should set output at such a level that marginal revenue equals marginal costs. Using our study of costs in the previous section, we find the situation illustrated below:

If the market price changes, the firm changes their level of output, always supplying output at the level where MR = SMC. So, in the short term, the short-run marginal cost curve represents the firms short-run supply curve, that is how much output they will supply at any given price. If however the price falls below their SAVC they should leave the market, so their short-run supply curve starts at the intersection point of SMC and SAVC.

If we add all of the SMCs in the market, then the equilibrium price is based on overall market demand’s intersection with this aggregate SMC.

So why is there a change from short-run to long-run? Well, the diagram below shows that where the SMC’s intersection with the demand curve (i.e. the price point) is above the SATC, the firm is making supernormal profits:

These supernormal profits will attract new firms to enter the market, which will cause the market supply curve to shift to the right, pushing price downwards, to the point where the firm is no longer making supernormal profits.

We consider below the impact on an increase in demand for a product (perhaps due to new positive aspects of it being discovered:

Note that the industry long-run supply curve (LRS) is horizontal at the equilibrium price, which is the minimum point of the long-run average cost curve for the typical firm in the industry.

So what is so good about a perfectly competitive market?

Well, it forces productive efficiency (in the long run) as firms must operate at minimum average cost in order to remain in the market. It also achieves allocative efficiency, by keeping the price equal to marginal cost.

Exercise

Monopoly

Strictly speaking, a monopoly is a market with a single seller of a good, however in practice, if a single firm dominates a market, they may be able to act as if they were the only firm – a dominant monopoly. The assumptions of a monopoly model are as follows:

- There is a single seller of a good;

- There are no substitutes for the good (actual or potential);

- There are barriers to entry into the market;

- The firm aims to maximise profits.

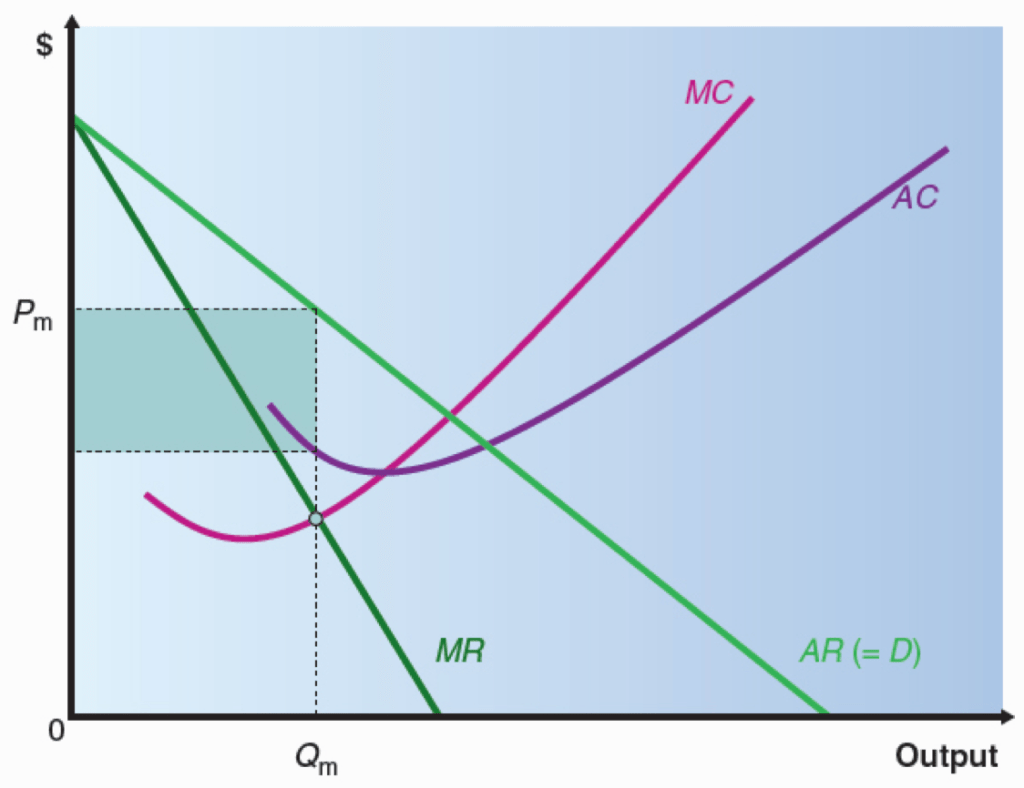

A monopoly firm faces the demand curve directly, so their demand curve is not horizontal, but slopes downwards and shows average revenue. As well as making decisions about output they can make decisions about price, although they are constrained by market demand. Below is a reminder of the level of elasticity at different points on the demand curve:

As with markets in perfect competition, a monopolist will choose to produce at a level of output where marginal revenue equals marginal cost, Qm on the diagram below:

As shown (the rectangle), this allows supernormal profits, and the barriers to entry ensure that these supernormal profits continue.

Exercise

Monopolies can occur for several reasons. The authorities can create one by requiring a licence for certain trades (e.g. the former Post Office in the UK). A patent can also create one. Patents help encourage R&D by preventing other firms benefiting from the investment one firm has made in R&D, however if a firm has an exclusive patent to produce a product, this puts them in a monopoly position for the lifetime of the patent. The level of investment in technology in an industry, e.g. oil production and space exploration, can also determine a market as a monopoly. Also a market with continued economies of scale will allow the largest firm to always produce at lower cost than smaller firms, which can also lead to a monopoly (known as a natural monopoly).

Productive efficiency is unlikely in a monopoly, as the firm will only produce at the minimum point of long-run average cost if this point coincidentally intersect the marginal revenue curve. Allocative efficiency also doesn’t occur, as marginal revenue will typically be below average revenue (i.e. price), so the price will be set above marginal cost.

Monopolistic Competition

Monopolistic competition is a market that shares some characteristics of monopoly and some of perfect competition. There is typically some level of product differentiation, a strategy adopted by firms to distinguish their product as being different from their competitors’. Typical such markets include fast-food outlets and travel agencies.

Product differentiation gives firms some influence over price. To achieve this they will often use advertising to develop brand loyalty. The other firms producing similar goods means that each firm’s product has substitutes, keeping demand relatively (although not perfectly) price elastic.

Typically there are no significant barriers to entry in the market, meaning that supernormal profits will attract new competitors. We say that the concentration ratio in the industry is low, meaning that a price change by one firm will have negligible impact on the demand for its rivals’ products.

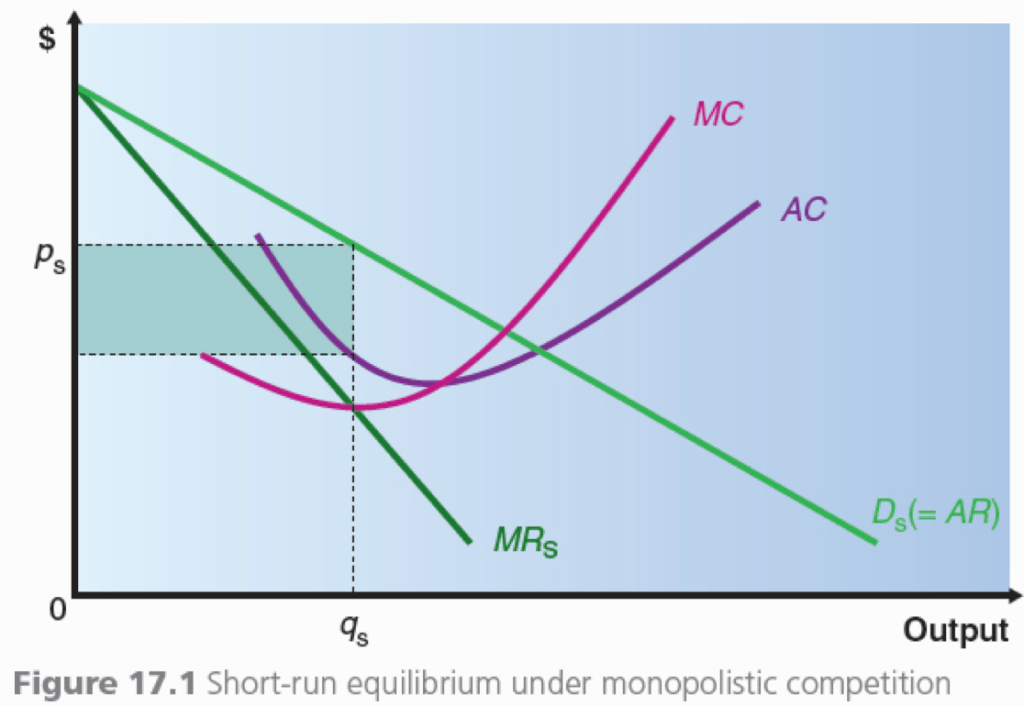

Below we look at short-run equilibrium in a market under monopolistic competition:

The MC and AC curves represent costs for a typical firm in the industry. To maximise revenue, they will produce a level of output where MRS=MC. As we see in the shaded area above, setting the price at this point leads to some supernormal profits, similar to what we saw with a monopoly.

This is of course only the short-run curve, because these supernormal profits will attract new entrants. As the new firms produce differentiated products, this will affect the demand curve for the firm being considered’s products, shifting it to the left as they attract away some customers, and changing its shape as the availability of substitutes increases.

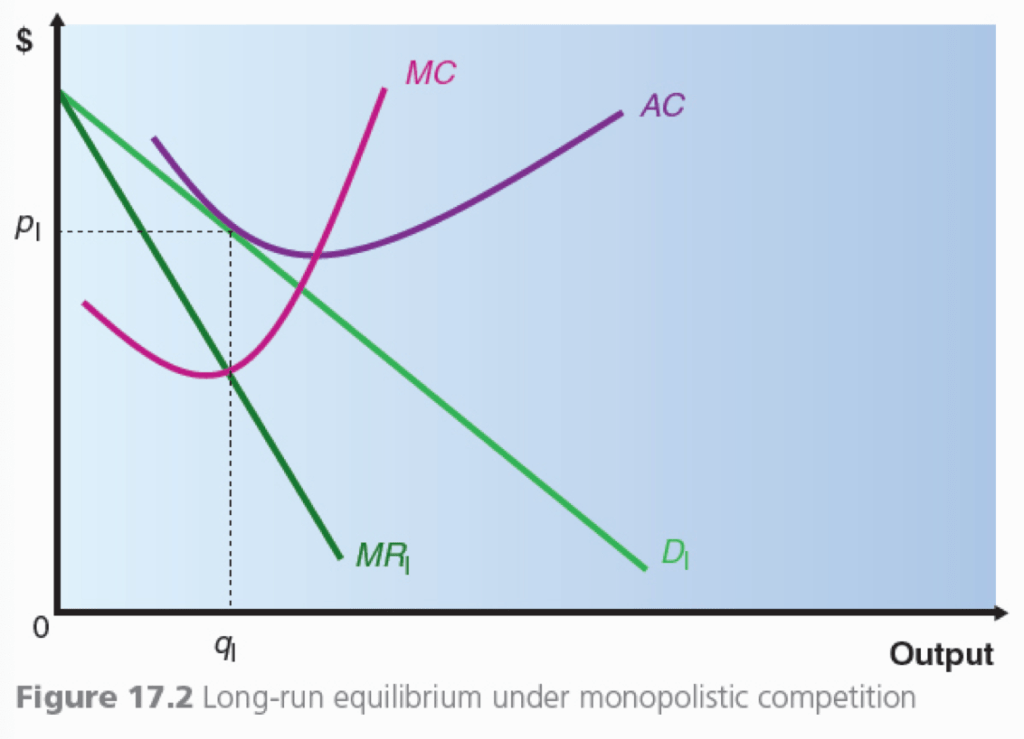

We consider the long-run below:

Here we see that at the price point where marginal revenue is equal to marginal costs, the average costs curve is tangent to the demand curve, meaning that average costs are equal to average revenue and so the firm is making normal profits (just covering their opportunity costs), which takes away the incentive for more firms to join the market.

We can see that neither productive efficiency nor allocative efficiency are achieved, because average costs are not minimised (so productive efficiency is not achieved) and the price charged is above the marginal cost (so allocative efficiency is not achieved).

It could be argued that product differentiation damages society’s total welfare, as it keeps demand curves downwards sloping, although this could be argued against, as people’s willingness to pay a premium suggests they have a preference for certain brands and so benefit from having greater freedom of choice. The use of advertising can also be seen as a problem with the market as generating unnecessary costs, although it may reduce inefficiency compared with a monopoly.

Exercise

Task – Monopolistic Competition

Advantages & Disadvantages of Monopolistic Competition

Task – Product Differentiation

Oligopoly

An oligopoly (the most common form of market structure) is a market with relatively few firms, in which each firm must take account of the behaviour and likely behaviour of their rival firms (consider examples such as cinema chains, or national newspapers).

We can measure the concentration ratio of an oligopoly by looking at the proportion of a market’s output that is generated by a specified number of firms (typically 4 – 8).

Due to the different strategies that firms may take in an oligopoly, there are various ways that such a market can be modelled. Oligopolies are likely to develop in markets where there are economies of scale; these make it difficult for too many firms to enter the market.

Firms in an oligopoly may be rivalrous or cooperative with each other, which respectively leads a market towards the competitive or the monopoly ends of the spectrum.

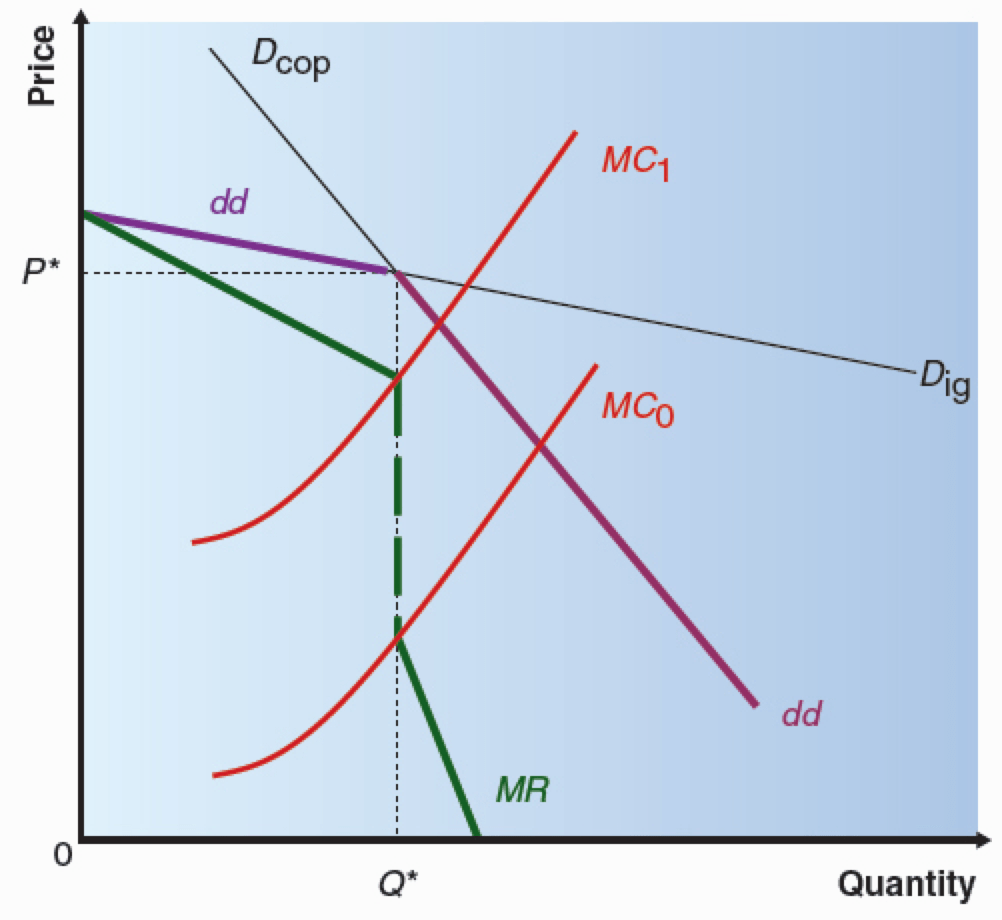

In the US in the 1930s Paul Sweezy developed the kinked demand curve model based on firms in an oligopoly trying to anticipate the reactions of their rivals. It works on the assumption that if a firm increases their price, competitors are not likely to follow their action, whereas if they reduce their price, their competitors will feel obliged to do so too. This model is shown below:

Suppose that a firm is currently selling quantity Q* at price P*. Their problem is that they only know about that on point on the demand curve. Dig shows the demand curve if other firms ignore a price change by them and Dcop shows the demand curve if other firms will copy a price change by them. The firm may consider that rivals will ignore a price increase (as this won’t threaten their market share), but copy a price decrease (as this would threaten their market share), which would lead to a kinked demand curve, as shown by purple line dd.

Due to the discontinuity in the marginal revenue curve shown above, the model predicts that in this situation a firm has a strong incentive to do nothing, even if costs increase.

Task – Oligopoly

Task

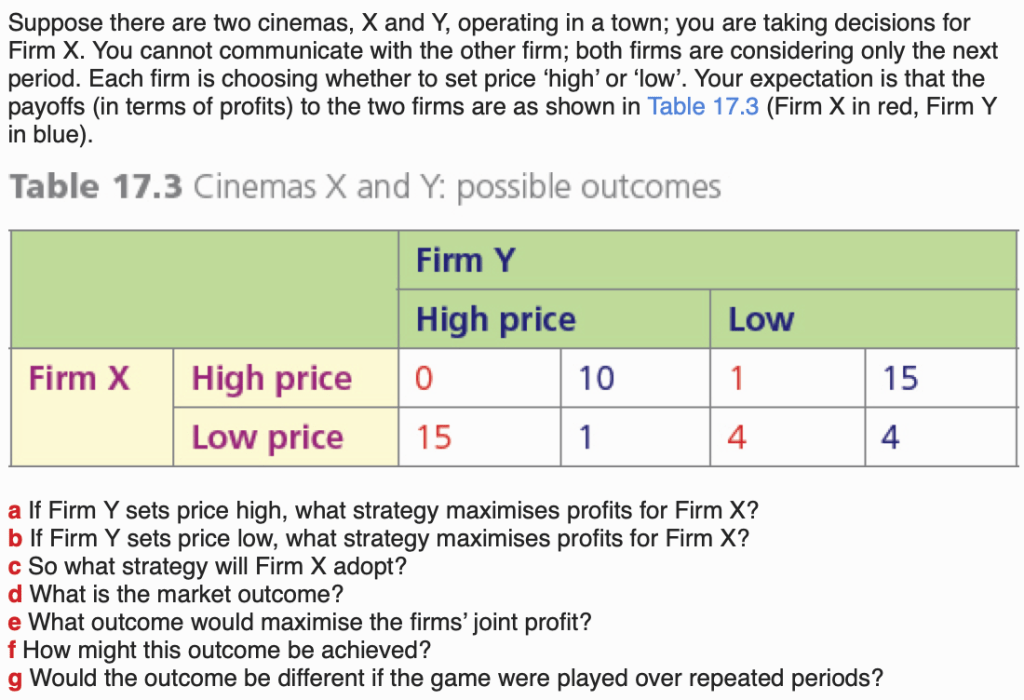

Game theory

Game theory is a method of modelling the strategic interaction between firms in an oligopoly. The most famous game, with multiply applications in economics, is the prisoners’ dilemma, based on lectures by Albert Tucker at Princeton University. In this dilemma, two prisoners have the option of providing evidence to the state of the guilt of the other prisoner. But they don’t know what the choice of the other prisoner will be. We can model this by saying that if one prisoner gives evidence and the other doesn’t, they will get 0 years in jail and the other will get 15 years in jail. If both prisoners give evidence then they will both get 10 years in jail. If neither prisoner gives evidence then they will both get 5 years in jail. This is tabulated below, with Al’s years served in red and Des’s years served in blue for each of the possible situations:

In game theory, a dominant strategy is a strategy that will give the best outcome regardless of what the other players choose. As we see in the table above, “confessing”, that is, giving evidence on the other party, is the dominant strategy, because it will give a better outcome regardless of the other party’s decision.

Game theorists refer to a maximin strategy if a player makes a decision that seeks to ensure that in the worst situation they have the least worse outcome, and a maximax strategy if a player makes a decision that seeks to ensure that in the best situation they have the best possible outcome. In the examples provided here, the dominant strategy achieves the maximin and the maximax criteria at the same time.

To apply this to economics, imagine two firms in a market where each firm can choose a high or low level of production output. If they both choose low production output, they will both make $2m, whereas if they both choose high production output they will both make $1m. If one chooses low production output and the other high output they will make relative amounts of $0m and $3m.

Again, although the best outcome for both comes from them both choosing low output, the dominant strategy for each firm individually is to choose high output. So, both will choose high output. Furthermore, when they observe their counterparts decision they will feel justified in their decision and have no incentive to change it. This is known as Nash equilibrium, a situation whereby each player’s chosen strategy maximises payoffs given the other player’s choice, so no player has an incentive to change their strategy.

In reality, “games” are of course much more complicated, and there are also non-pricing strategies that companies can use (e.g. in the airline market offering additional leg room or greater baggage allowances), and games are not typically zero-sum, like the ones considered here (i.e. a gain for one firm doesn’t necessarily mean a loss for another). Game theory also assumes “rational economic behaviour” and doesn’t take into account behavioural economics.

Exercise

The examples above show how forming a cartel (an agreement between firms on price and output with the intention of maximising their joint profits) can be advantageous to each of the firms in it. However with a cartel there is always the temptation for a cartel member to cheat (as this is an unpoliced environment) and achieve additional market share at the expense of the other firms in the cartel. In most countries (Hong Kong is a rare exception) cartels are illegal. A famous international example of a cartel is the Organisation of Petroleum Exporting Companies (OPEC).

Certain conditions are necessary for a cartel to operate successfully:

- Limited number of firms in an industry, who all belong to the cartel;

- Similar cost structures for all firms;

- High barriers to entry preventing new firms entering industry;

- Firms all obey the cartels rules;

- Market is stable (i.e. not recessionary, especially if product has high YED);

- Firms produce very similar or identical products.

Although cartels are typically illegal, firms often look at other alternatives such as loose strategic alliances, such as happens with the airlines whereby they share airport lounges through joint club such as “One World Alliance” and “Star Alliance”. These do impact on competition however, and regulators have interfered with such alliances, for instance preventing British Airways and American Airlines from allying under the terms that they initially intended. Tacit collusion can occur when firms refrain from competing on price, but without any communication or formal agreement between them.

Exercise – Price War

Exercise – Types of market

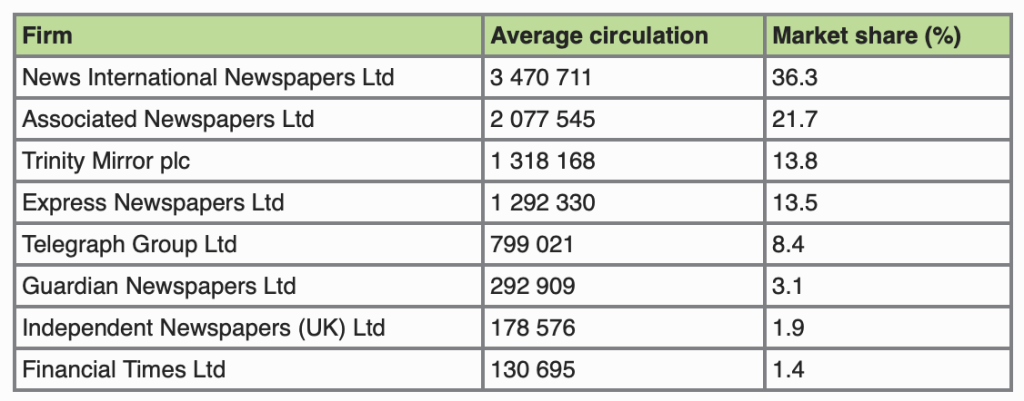

One way of identifying where markets lie on the spectrum from monopoly to perfect competition is to calculate an n-firm concentration ratio, which is a measure of the market share of the largest n firms in an industry. This is typically calculated based on output, but could also be calculated by numbers employed. We use the following table to consider this measure:

In this example, the 3-firm concentration ratio is 71.8%. Sometimes a more granular approach is needed though, as we could argue that the Sun (part of News International) and the Financial Times are not really part of the same market.

Economies of scale heavily impact the structure of a market, as significant economies of scale will tend to entrench a largest firm in a market, especially when combined with learning-by-doing effects.

If a market relies on raw materials, ownership of those raw materials and also have a large impact on a firms ability to achieve a dominant position in a market, as was the case with diamond producer De Beers during the 20th century.

Extensive advertising can also entrench a dominant position and server as a barrier to entry. Coca-Cola and Pepsi are good examples of this, with any entrant into the fizzy drinks market requiring to invest a considerable amount in advertising in order for them to be seen by customers as a serious contender in these heavily dominated markets.

Exercise

Contestable Market

The idea of a contestable market is subtly different and level of contestability is not precisely a market structure. The concept was developed by William Baumol relating to domestic US air transport in the 1970s and relates to low barriers to entry. He suggested that rather than heavily regulating airlines, acting to reduce barriers to entry would lead to a drop in price. His ideas were implemented by the US government in 1979 leading to a reduction in fares on many routes and helped influence UK subsequent policies involving privatising and deregulating transportation systems and public sector industries.

A market is perfectly contestable if:

- There is a pool of potential entrants seeking to enter the market;

- Entry and exit are costless;

- All firms are subject to the same regulations and have access to the same technology;

- Mechanisms help prohibit limit pricing, as existing firms have lower costs than potential entrants;

- Firms already in the market are vulnerable to “hit and run” competition.

As long as entry is free and exit is costless, theoretically, any market structure could be a perfectly contestable market.

Final Task