Introductory Task

Section 1: Measuring Exchange Rates

We can measure the price of a currency in several ways, such as measuring it by how much it costs in another currency, by how much it can buy in another country, or in terms of a basket of currencies.

Nominal and Real Exchange Rates

Nominal Foreign Exchange Rate is the price of one currency in terms of another currency. For example, 3 GEL may buy 1 USD.

The Real Foreign Exchange Rate uses price changes as well as the exchange rate to indicate the competitiveness of a country’s products in global market. If a country has a high inflation rate, then export prices may be increasing despite a fall in their foreign exchange rate. We can say that it is the currency’s value in terms of its real purchasing power.

An increase in a country’s real exchange rate means that their products are becoming more expensive relative to other countries, and will typically lead to an increase in imports and a reduction on exports. The real exchange rate gives better information on the impact on the current account balance than the nominal rate.

Task 1

Suppose that the US dollar : Mexiacan peso exchange rate is $1 = 20 pesos and that the US price index is 144 and the Mexican price index 120.

- Calculate the real exchange rate;

- Decide whether the dollar is undervalued or overvalued.

Trade-Weighted Exchange Rate

A country will trade with a variety of different countries and often its currency will rise in value against some whilst falling against others. The trade-weighted exchange rate is a useful measure, in index form, of the price of the currency against a basket of currencies. These currencies are weighted according to their relative importance in the country’s trade.

Section 2: Determination of Exchange Rates

Exchange rates can be determined by free market forces, by a government, or by a combination of both. In the majority of governments, their central banks allow market forces to play a large role in determining their exchange rates, only intervening if there are large fluctuations.

Fixed Exchange Rate System

In a fixed exchange rate system the government determines the price of the currency. The central bank then maintains that rate, either by direct intervention (buying and selling currency) or by trying to influence the market demand for and supply of the currency (e.g. by changing the rate of interest).

Below this is illustrated for UAE’s Dirham against the US dollar. If the supply of Dirham increase from S to S1, then the central bank could by enough Dirham to shift the demand curve from D to D1, maintaining the exchange rata at 1 dirham: $0.25

Clearly it will be easier for a central bank to maintain a fixed exchange rate if that rate is close to the long-run equilibrium value of the currency. If, instead, they overvalue the exchange rate, the central bank can be at risk of running out of reserves trying to maintain the exchange rate at a level that does not reflect its market price.

One downside of a fixed exchange rate is the need to keep reserves. This represents an opportunity costs, as the gold or foreign currency being held could be used for other purposes.

Another risk is that a government may sacrifice other policy objectives to maintain a fixed exchange rate (e.g. raising an interest rate to increase demand for a currency may at the same time reduce aggregate demand and increase unemployment).

Due to market pressures, the rate at which a currency is fixed may need to be changed over time. This is called a devaluation or a revaluation depending on whether the rate is reduced or increased.

On the positive side, a fixed exchange rate offers certainty, which can promote international trade and investment. It also imposes discipline on a government to keep inflation low, to avoid downward pressure on the exchange rate.

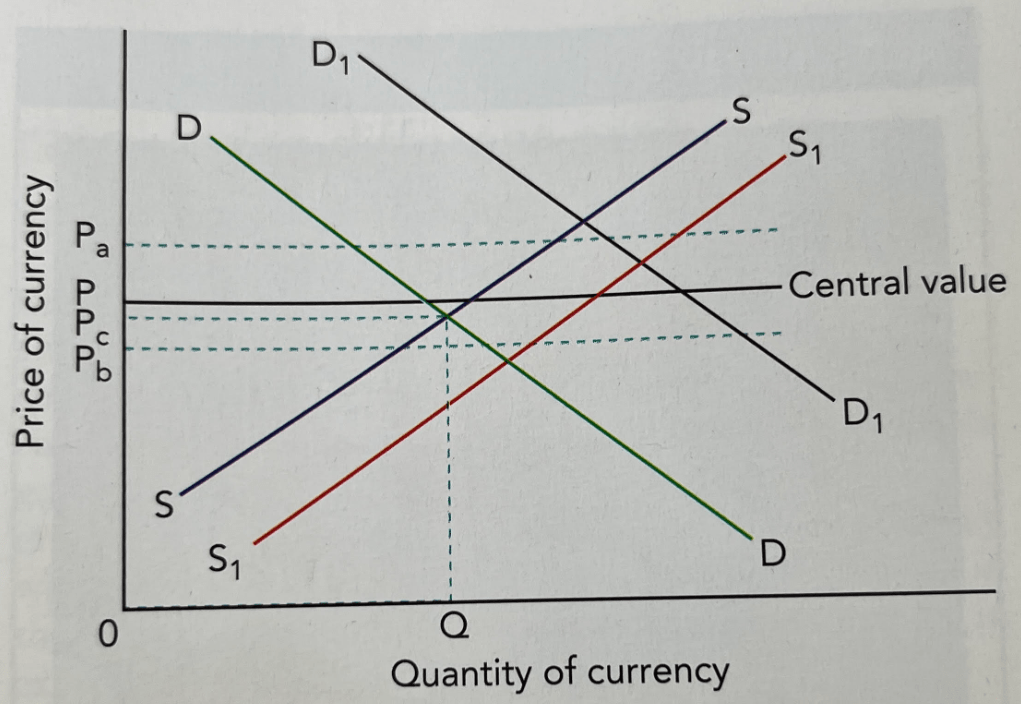

Managed Exchange Rate System

In a managed system, a government typically allows the exchange rate to be determined by market forces within given limits. Below we see where the government has sent a central value of P, an upper limit of Pa and a lower limit of Pb:

If the exchange rate remains within the limits (e.g. at Pc), no action is taken. If demand were to rise to D1, then the central bank would sell domestic currency to increase supply to S1, keeping it within the limits.

Task 1

Section 3. Changes in Exchange Rate under different Exchange Rate Systems

The main reason that demand for a currency increases is due to an increase in demand for the country’s goods and services, increases in direct and portfolio investment in the country and speculation that the currency’s price will rise in the future.

Some reasons a government might instruct its central bank to bring about a revaluation of a currency are:

- They may think that there is too much upward pressure on the currency and not want to sell large quantities of it to keep the price down as this would add to the money supply;

- They may want tor reduce inflationary pressure by reducing the price of imports and also thus putting pressure on domestic industries to become more internationally competitive.

Task

Section 4. Impact on the external economy of changing exchange rates

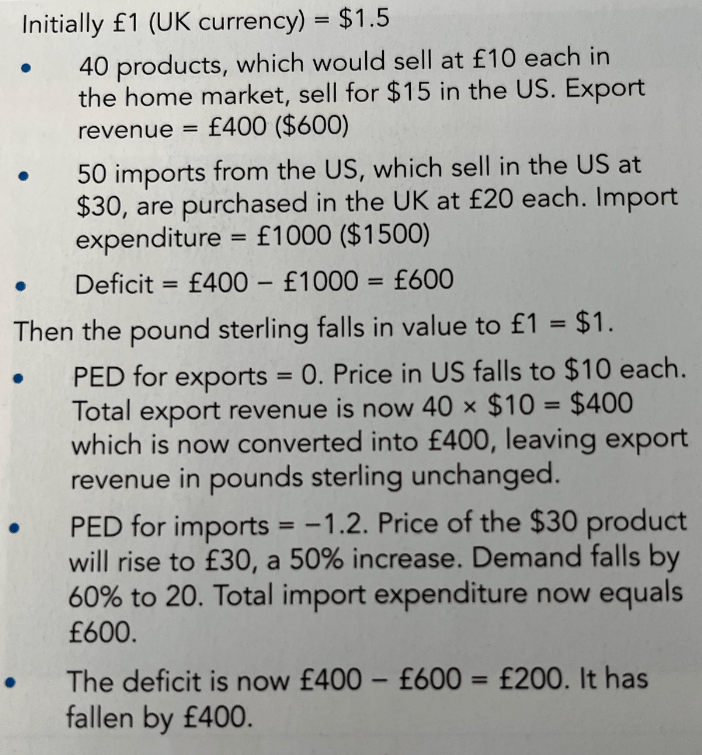

Any change in the exchange rate on the current account balance will be influenced by the price elasticity of demand of exports and imports. As we learned at AS level, the Marshall-Lerner condtion states that the combined elasticities must be greater than 1 for the current account balance to be improved (or worsened) by a change in the exchange rate. The table below demonstrates the Marshall Lerner condition for a fall in the exchange rate:

A larger combined PED for exports and imports will mean that less of a fall in the exchange rate will be required to improve the current account position. If the combined PED is less than 1, then a revaluation of the exchange rate would be a more suitable strategy.

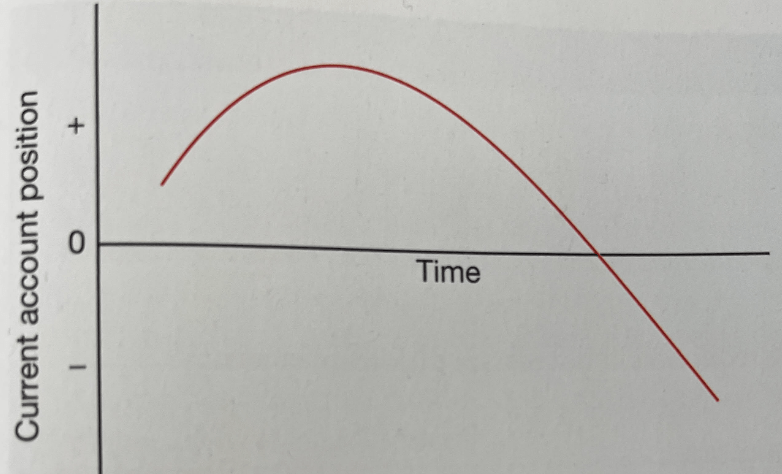

Related to the Marshall-Lerner condition is the J curve effect. This describes how a fall in the exchange rate will worsen the current account position before it starts to improve it, because in the short run, demand for imports and exports tends to be relatively inelastic, as time is needed to recognise that prices have changed and then to search for alternative products. In the long-term however, demand becomes more elastic and the current account position can move from deficit to surplus, as demonstrated below:

The J curve is upside down when we consider a rise in the exchange rate, causing an increased surplus in the short term before reducing it in the long term:

Task

In pairs, prepare a leaflet for AS Economics students studying exchange rates on whether your country’s central bank should seek to increase the value of your country’s currency, reduce its value, or leave it unchanged.