1. What is marginal cost?

A the difference between the total cost of producing n units and n – 1 units of output

B the difference between the average variable cost of producing n units and n – 1 units of

output

C the difference between the average total cost of producing n units and n – 1 units of output

D the average fixed cost of producing one more unit of output

2. The table shows the production and total cost of a firm.

| Production (tonnes) | Total cost ($) |

| 0 | 20 |

| 1 | 30 |

| 2 | 35 |

| 3 | 40 |

| 4 | 45 |

| 5 | 50 |

What is the average variable cost of producing 5 tonnes of output?

A $4 B $5 C $6 D $10

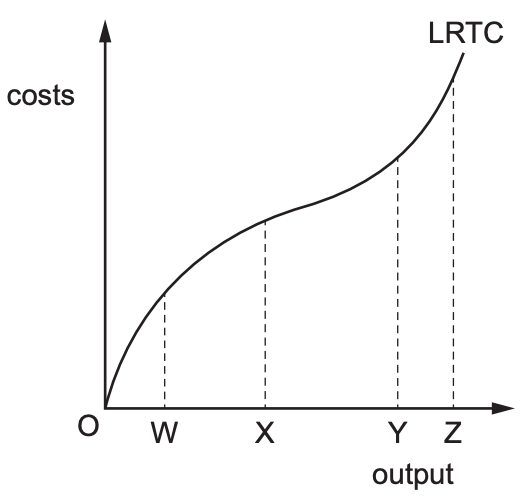

3. The diagram shows the long-run total cost (LRTC) curve of a firm.

At which output is the long-run average total cost at its minimum?

A OW B OX C OY D OZ

4. Which combination of statements about small firms and large firms is correct?

| Small firms | Large firms | |

| A | Are more common in manufacturing than in services | Face high barriers to exit |

| B | Are more numerous than large ones | Do not experience diseconomies of scale |

| C | Can do well when each item produced must be different | May arise from internal growth or mergers |

| D | Cannot have any monopoly power | Cannot earn supernormal profits |

5. Why might the long-run equilibrium of a profit-maximising firm in a monopolistically competitive

market differ from its short-run equilibrium?

A Advertising expenditure is possible.

B There are low barriers to entry.

C Firms experience diminishing returns.

D Innovation reduces the monopoly power of firms.