Introductory Task

Nationalisation and Privatisation

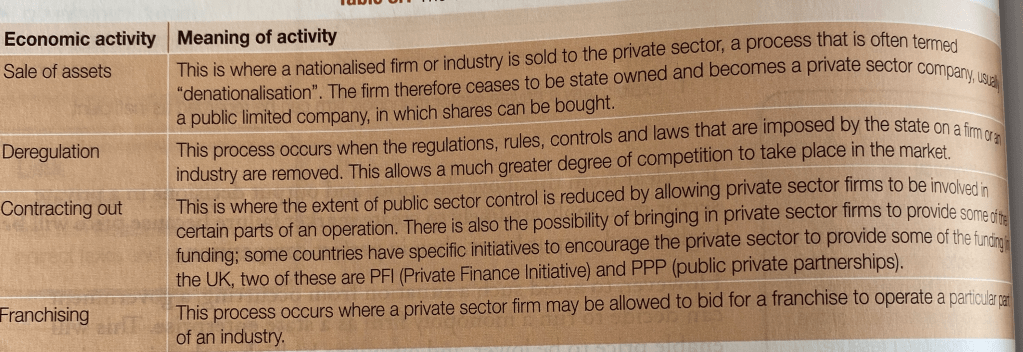

During AS level we contrasted nationalisation, which involves the government operating a monopoly, with privatisation. Some of the types of privatisation are listed below, followed by some tasks to help us think about it.

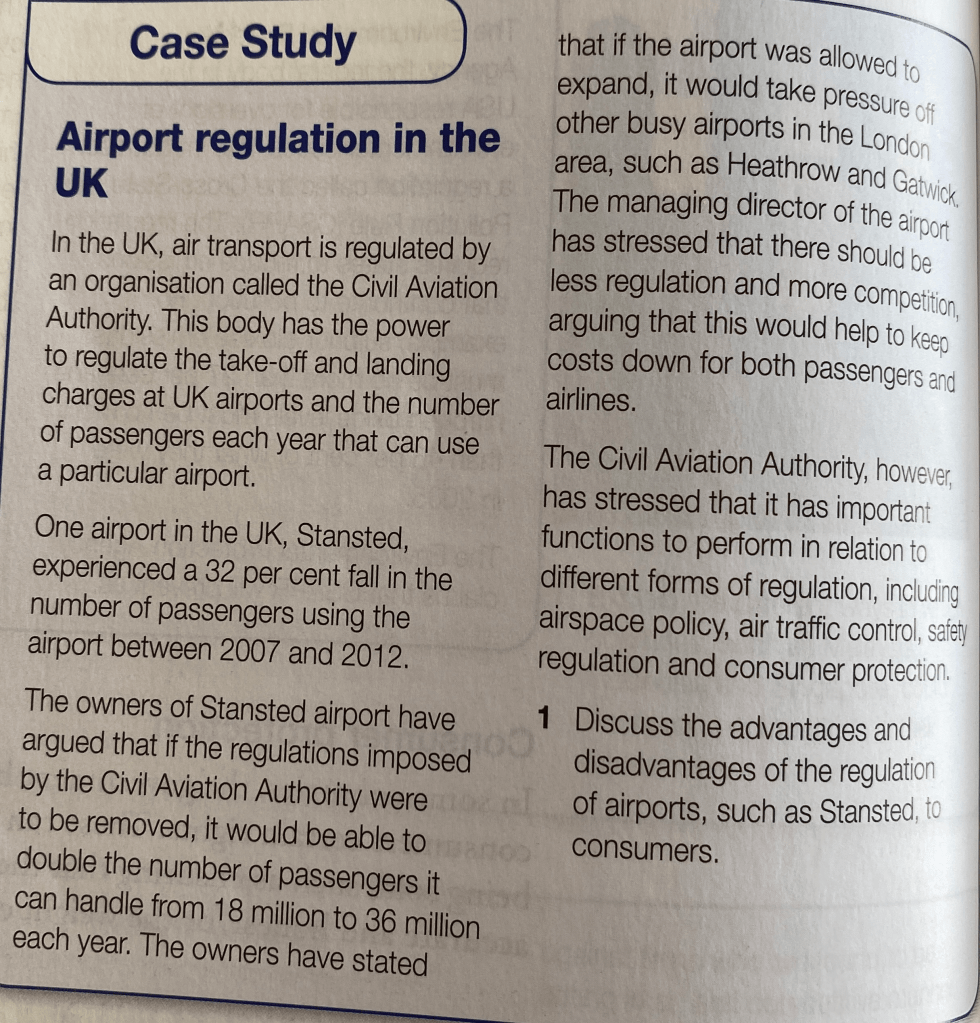

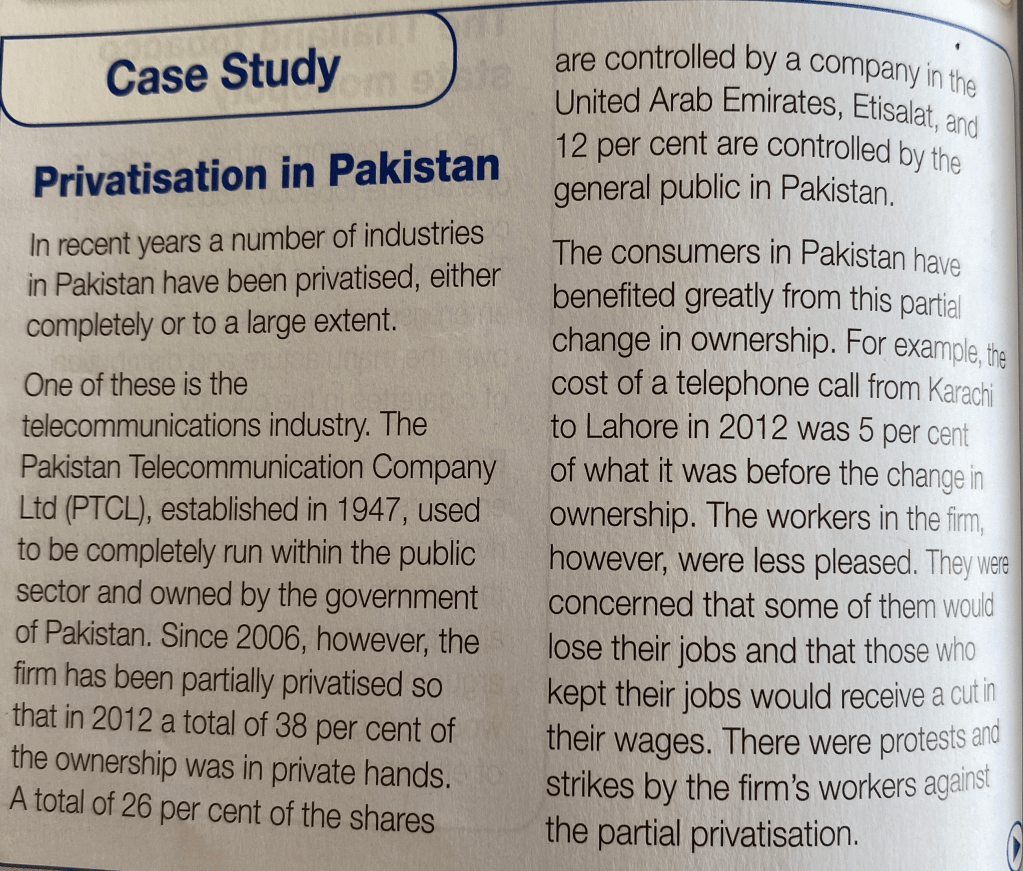

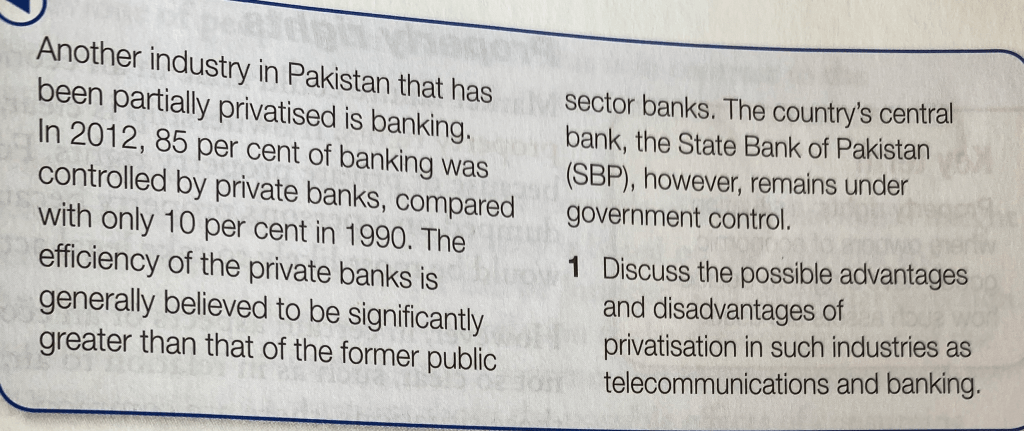

Task 1 – Privatisation

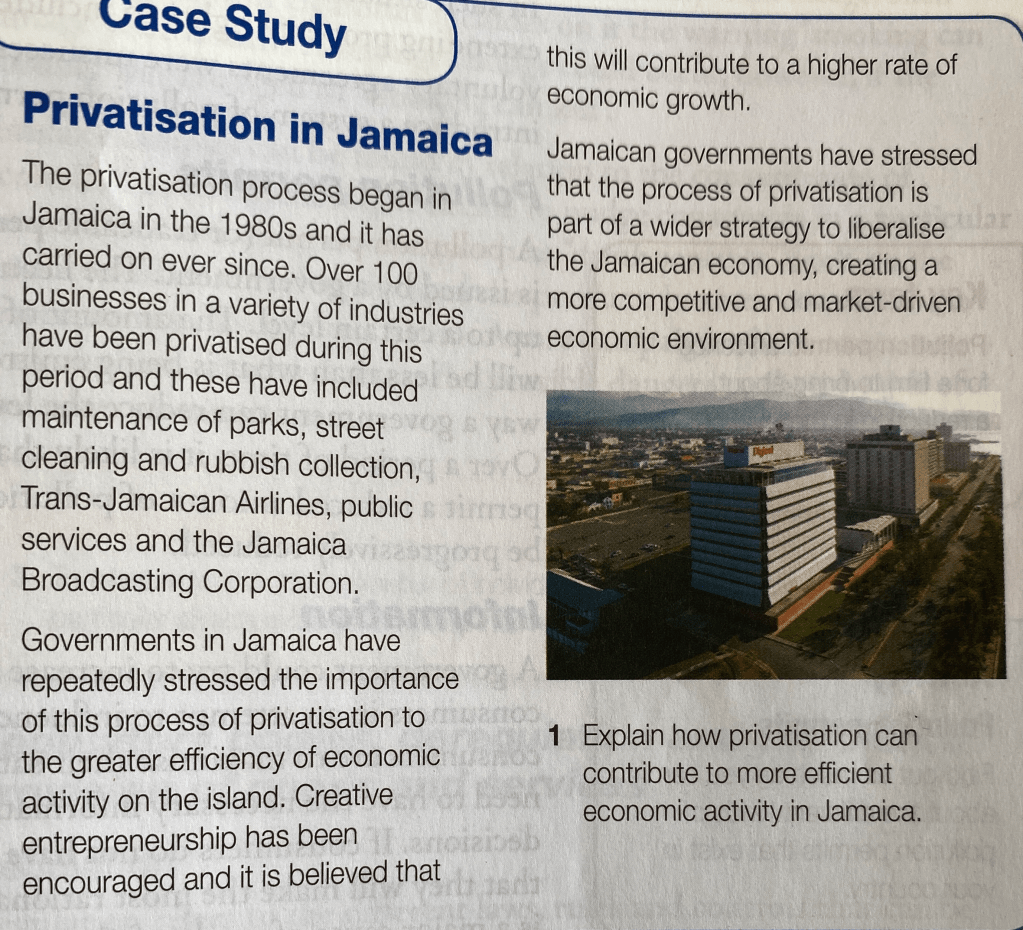

Task 2 – Privatisation

Market Failure

The free-market mechanism sometimes doesn’t produce the best allocation of resources for society as a whole, e.g. with a negative production externality such as pollution, marginal social costs exceed marginal private costs, so firms ‘overproduce’ pollution.

Merit & Demerit Goods

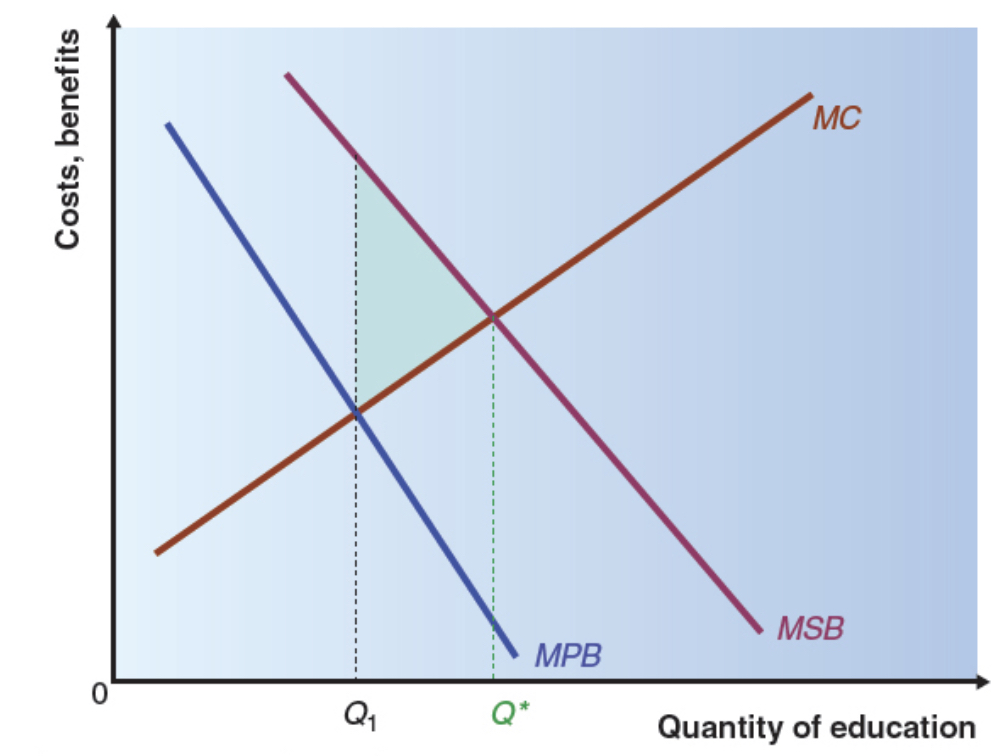

Let’s consider education as an example of a merit good. Most countries mandate compulsory attendance at school for a specified number of years. This is partly because education is a merit good and provides benefits to society in excess of those perceived by individuals. In the diagram below, we show that the marginal social benefit (MSB) is higher than the marginal private benefit (MPB), so whilst the free market would produce only Q1 of the good, society as a whole would prefer if Q* of the good was produced.

We can also argue that there are positive externality effects if educated workers are able to better cooperate with each other and that individuals may fail to demand sufficient education because of information failure (i.e. they don’t perceive that full benefits that arise from education).

We should also consider equity issues related to education, as education typically leads to higher lifetime earnings, but the cost of education can be prohibitive for low-income households. One way that such issues have been addressed has been by the use of student loan schemes, lending money on more favourable terms than typically available in the market.

The definition of a merit good is highly normative, but can be considered to include museums, libraries and art galleries.

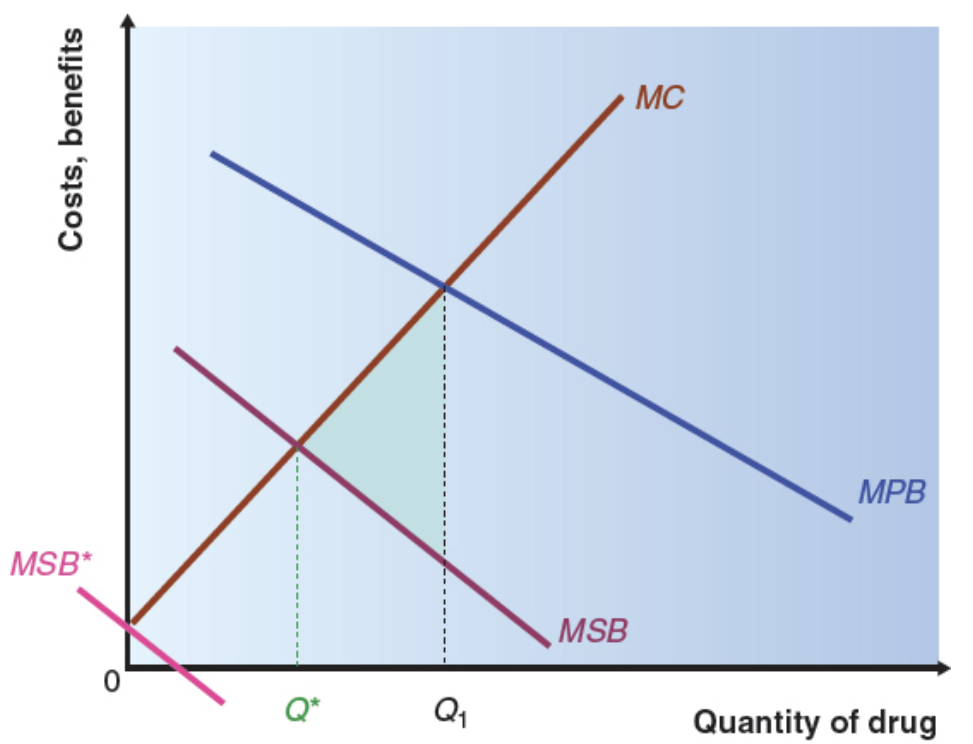

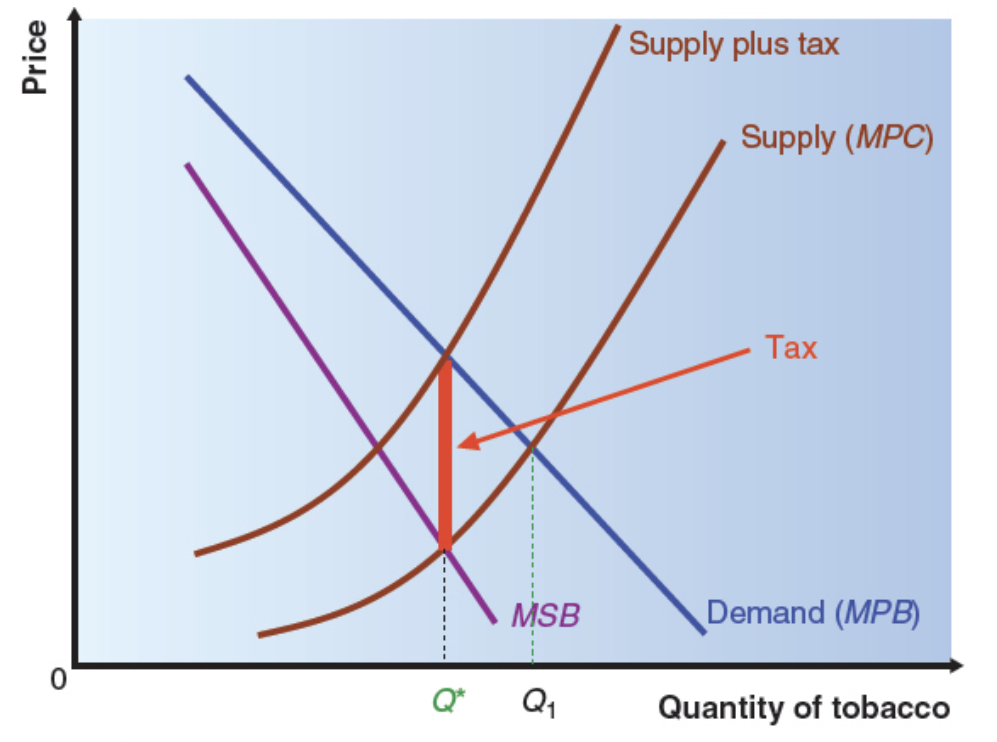

Let’s consider the sales of opiate drugs as an example of a demerit good. In the diagram below we show that MPB is much higher than MSB and so consumption is at Q1 whereas society would like it to be at Q*.

Again, this could be described as an information problem, with consumers having insufficient information about the dangers of addiction and thus overvaluing the drug. The government could tackle such an information failure through education campaigns. The below diagram shows the market for tobacco, showing how a tax can be used to reduce the quantity consumed form the market equilibrium at Q1 to the desired level at Q*.

Externalities

An externality is some part of the cost or benefit associated with a transaction that is not reflected in the market price. When there are externalities, a free market will not lead to an optimum allocation of resources. One way to tackle this is to internalise an externality, that is to bring the externality into the market mechanism. Let’s consider how this could be achieved for the specific example of the negative production externality, pollution:

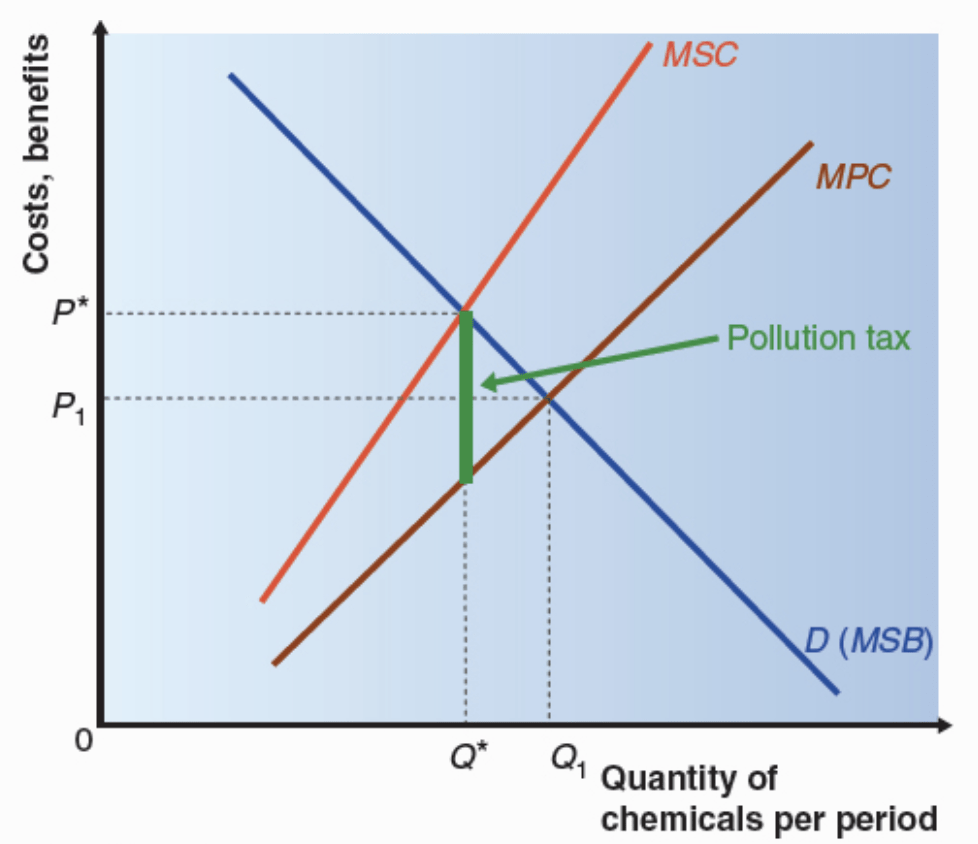

Firms producing chemicals with a process that emits toxic fumes will impose costs on society that the firms do not incur themselves (the marginal private costs felt by the firms are less than the marginal social costs inflicted on society). They will produce a total of Q1 and charge P1 to their customers. At this point, the marginal social benefit is less than the marginal social cost, so we could argue that too much of the product is being produced – it would be better for society if a quantity of Q* was produced, setting the price at P*.

The polluter pays principle tries to levy these costs on to the polluting firm. One option is to impose a tax, as shown above.

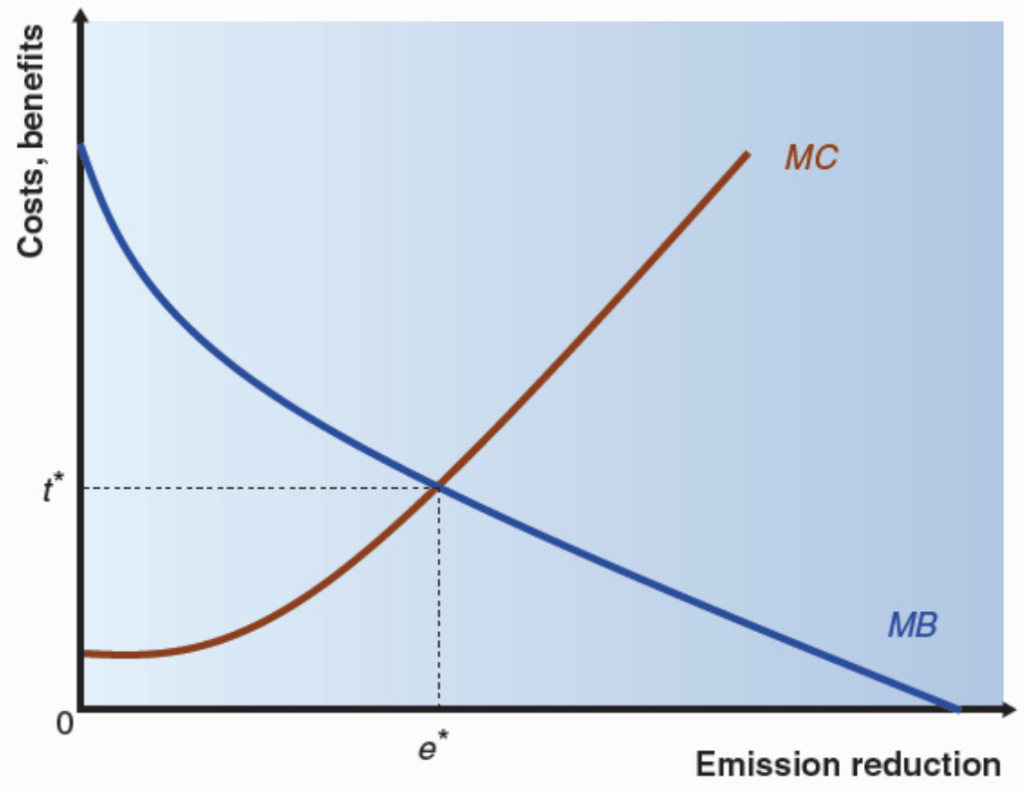

Another way to consider this is by looking at the marginal benefit and the marginal cost of reducing emissions, as shown below:

The optimum amount of reduction of a pollutant is found where the marginal social benefit of such reduction is equal to the marginal cost, i.e. e* on the diagram above. Setting a tax equal to t* will encourage the appropriate amount of emission reduction. Another alternative would be to impose regulations that prohibit emissions beyond e*. Either of these policies would be effective if the authorities have full information on marginal costs and benefits. This is difficult to measure with great precision though (both in terms of costs and benefits).

Another option is tradable pollution permits. The government can issue or sell permits to firms allowing a certain level of pollution. Then if a firm uses ‘cleaner methods’ and so don’t use up their full allocation, they can sell their polluting rights to other firms. This provides a good incentive to firms to reduce pollution. Effectively, this approach internalises the negative externality of pollution rather than overriding the market. Enforcement remains an issue, however, as such a system would require sanctions for non-compliance and a cost-effective method for checking the level of emissions.

Global warming is an important international issue that requires coordination of effort across countries. Various conferences have been held to try and tackle it. It is worth keeping up to date by reviewing news articles on the current situation in tackling this and what solutions are offered. I would also recommend the book “Economics for the Common Good” by French economics professor Jean Tirole that looks in detail at this and various other economic solutions for contemporary problems.

We should also be aware of the NIMBY (not in my back yard) problem that negative externalities are often not felt equally be different people. A new runway leading to planes flying low over one neighbourhood’s houses or a wind farm that obstructs the beautiful views from a certain village may be for the common good, but may cause local protests and discontent.

Task

You learn from the local newspaper that the local authority has chosen to locate a new landfill site for waste disposal alongside the park behind your home. What costs and benefits for society would result? Would these differ from your private costs and benefits? Would you object?

Property Rights

The workings of the economy depend upon a system of secure property rights. This is supported by the legal system.

Externalities often exist due to failings in the system of property rights. For instance, a factory that emits toxic fumes into a neighbourhood is interfering with the residents’ clean air. If the residents could be given property rights over the air they use, they could require the firm to compensate them for the costs inflicted. But the people in the neighbourhood would all be affected to different extents, due to wind direction and proximity to the factory, and so it becomes impossible in practical terms to assign property rights and internalise the pollution externality. Effectively the government takes over those property rights and acts a collective enforcer. In summary, as argued by Nobel prize winner Ronald Coase, externality effects can be internalised where property rights can be enforced without high associated transaction costs.

Nudge Theory

Economist Richard Thaler introduce the idea of nudge theory, which was very influential in affecting UK government policies during the 1990s and beyond. The idea is to influence consumers’ choices by providing information that “nudges” them towards making more effective decisions, often by reframing the debate. Hence stricter interventions and regulations can be avoided by encouraging consumer decisions that have better social outcomes.

Imperfect competition

In conditions of perfect competition, firms are fairly passive and respond to changes in consumer preference. Of course, in the real world firms do often have some power over their actions.

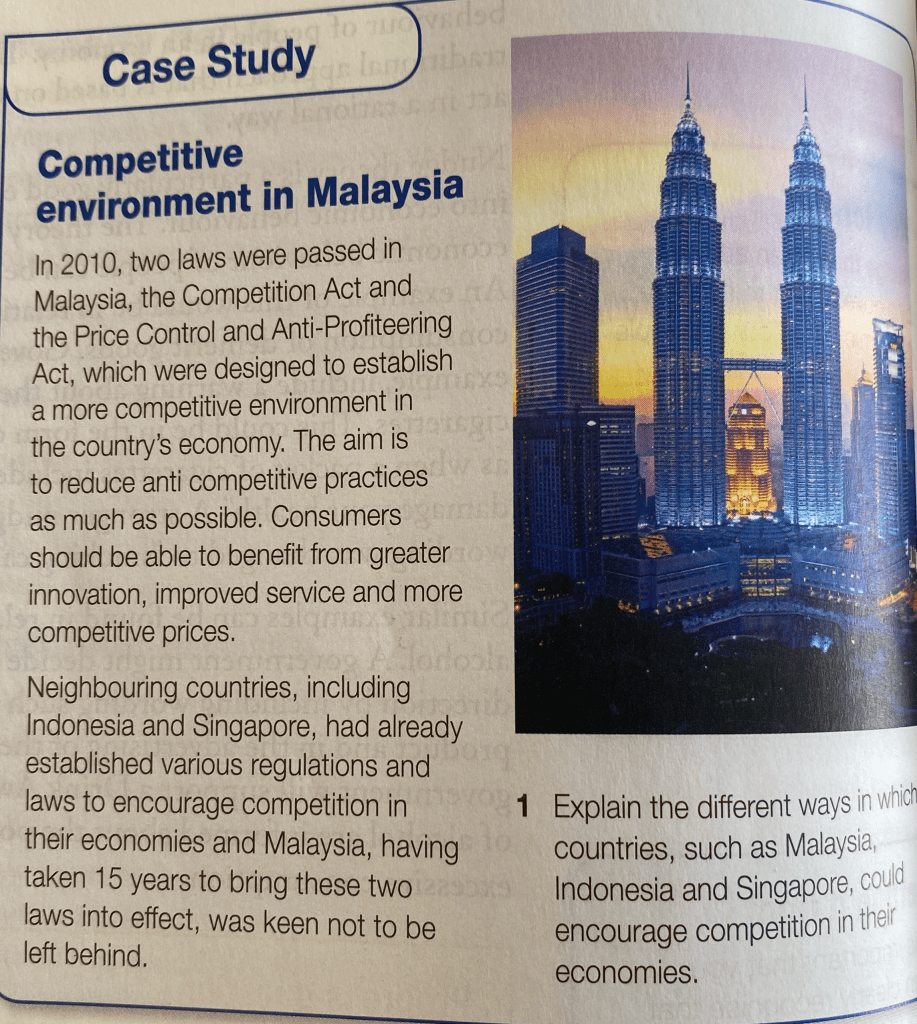

If a firm achieves a dominant position in a market, they may try to exploit their position at the expense of consumers (e.g. in 1998 when Microsoft controlled 95% of the worldwide market for PC operating systems, they were taken to court in the US accused of abusing their dominant position). Many countries have some kind of body responsible for protecting consumers against dominant firms, e.g. Competition and Markets Authority (UK), Competition Commission (Pakistan) and Malaysia Competition Commission (Malaysia).

Firms with a dominant position in a market can distort the allocation of resources, for instance by restricting output and raising market prices to a level above the marginal cost of production, causing customers to lose out in terms of allocative efficiency. From society’s perspective too little of the product is produced. We could consider this as a redistribution of producer surplus from consumers to producers. However, there is also a loss of consumer surplus that is not recoverable.

The market system relies on price acting as a reliable signal of consumer demand, so firms are attracted into the market when the prices are high and tend to leave it when prices are low. This depends upon competition between firms and the freedom to enter and exit markets. Barriers to entering a market, for instance, can give firms undue influence over the price, leading to less product being produced than is desirable for society.

Most countries have a competition policy, which seeks to encourage market efficiency and protect consumer interests. It is a delicate balance, because economies of scale mean that large firms can be more productively efficient, so the government shouldn’t seek to always fragment industries into smaller firms even if this does stimulate competition. Also, getting accurate information can be difficult, as prices are always fluctuating for many reasons, and not just because of abuse of market power.

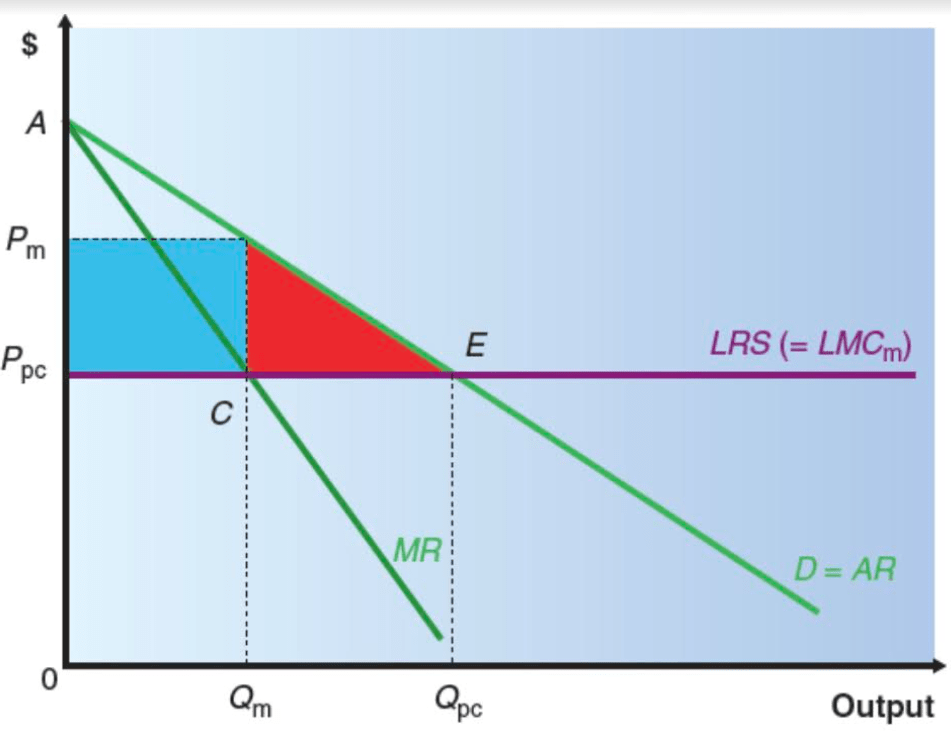

Let’s assume that an industry can operate either under perfect competition with many small firms, or as a “multi-plant” monopolist and that there is no cost difference. Then the long-run supply schedule (SRS) under perfect competition is, for the monopolist, their long-run marginal cost curve, so in long-run equilibrium the monopolist varies output by varying the number of plants it operates.

Under perfect competition, output would be set at Qpc and market price at Ppc. A monopolist would restrict output to Qm and raise the price to Pm. This reduces consumer surplus, by transferring the blue rectangle to the monopoly as profits and by the deadweight loss of the red triangle. The competition policy seeks to remove this deadweight loss, which is a cost on society.

Economists talk about a structure-conduct-performance paradigm, the idea that the structure of a market (i.e. the number of firms) determines how the firms in the market conduct themselves, which in turn determines how the market performs in terms of productive and allocative efficiency. We need to consider some issues related to this.

First we consider the assumption that cost conditions are the same under perfect competition as under monopoly. Due to economies of scale this will often not be true, as a monopoly firm will face lower cost conditions than apply under perfect competition.

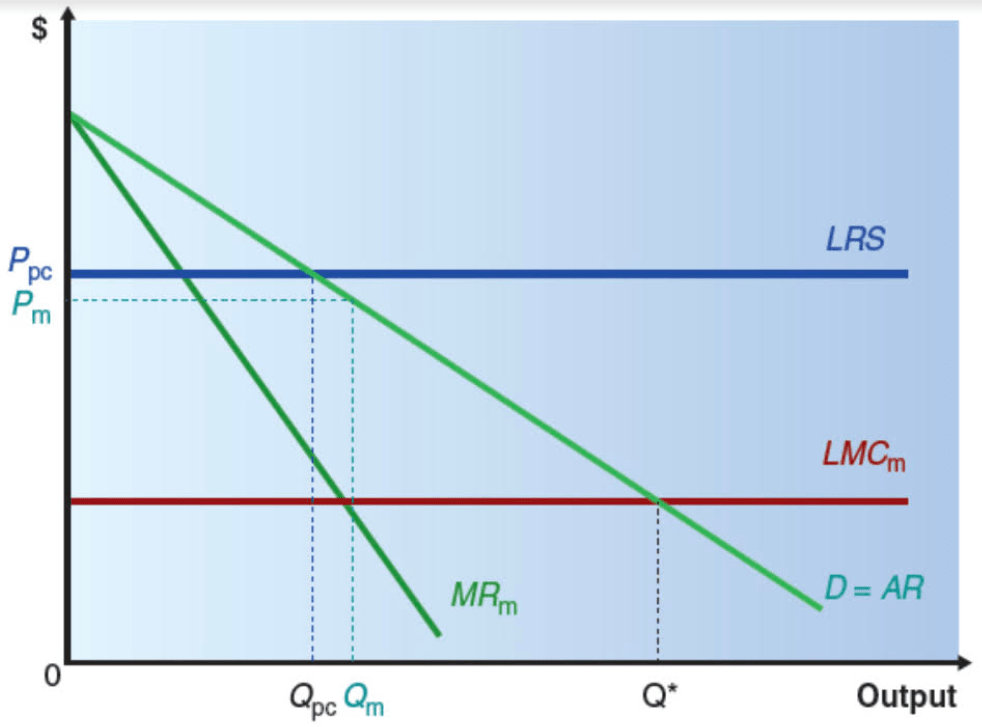

In the below diagram, LRS is the long-run supply schedule of an industry operating under perfect competition. The equilibrium point under perfect competition is output level Qpc and price Ppc. However a monopolist with a strong cost advantage able to produce at constant long-run marginal cost (LMCm) could maximise profit by choosing output Qm, where MRm equals LMCm and would sell at price Pm, thus producing more output at a lower price than a firm operating under perfect competition.

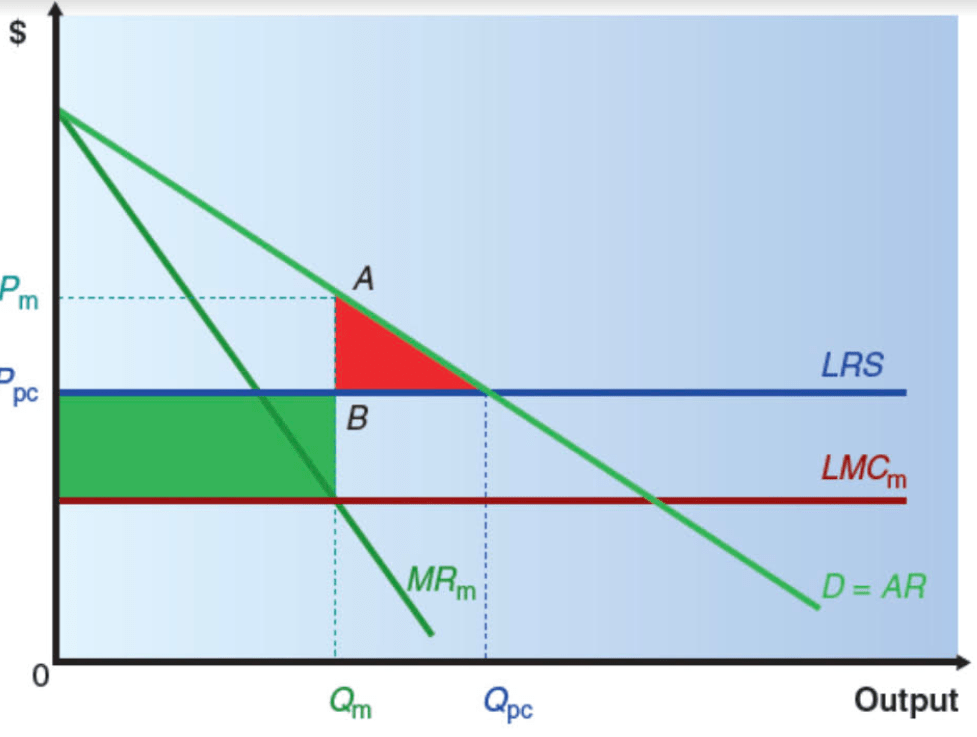

Although in the monopoly situation the market does not achieve allocative efficiency, the loss of allocative efficiency is offset by the improvements in productive efficiency achieved by the monopoly firm. Regulations forcing the monopolist to produce at Q* would have no incentives to operate efficiently. Joseph Shumpeter argues that monopoly profits benefit society by giving an incentive for innovation and allowing firms to engage in R&D.

A less extreme case is demonstrated below:

Here the deadweight loss is given by the red triangle, representing the allocative inefficiency of monopoly, however it is more than offset by the gain in productive efficiency represented by the green rectangle. This is part of monopoly profits that under perfect competition was part of production costs. Of course, in addition to whether society is better off overall, we should consider distribution of income. The area PmABPpc would be part of consumer surplus under perfect competition, but becomes part of the firm’s profits under monopoly.

Contestability is the idea that if the barriers to entry into the market are weak and the sunk costs of entry and exit are low then the monopoly firm will need to be competitive to discourage potential entrants. If a market is perfectly contestable, the firm may need to maintain a low price (i.e. not the profit-maximising level of output) to discourage entry.

It is not only monopolies that can influence price, but also markets with high concentration (a small number of firms each of a large size), i.e. oligopolies, which may collude and act as a joint monopoly. As previously though, we cannot assume that a concentrated market is always and necessarily and anti-competitive market.

Globalisation is also an important issue. Some economists believe that large domestic firms should be allowed to dominate the domestic market so they can then enjoy a competitive position in the global market. Others have suggested that a large domestic firm benefits more from facing international competition in the domestic market, which helps productive efficiency and thus better prepares it to cope with international competition.

Task

Discuss whether a concentrated market is necessarily anti-competitive.

Natural monopoly and privatisation

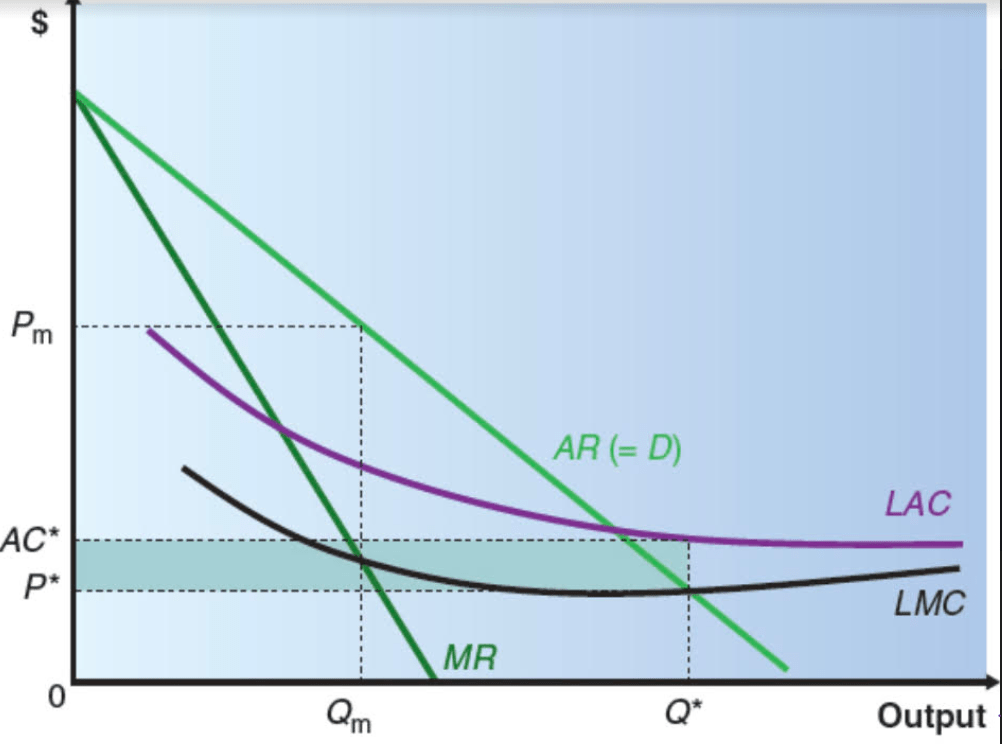

An industry with substantial economies of scale relative to market demand tends to end up as a monopoly, as the largest firm can always dominate the market and undercut smaller competitors. On the diagram below, if the monopolist chooses to maximise profits, it will set marginal revenue equal to marginal cost and produce Qm at price Pm:

Such industries typically have large fixed costs relative to marginal costs (e.g. railway networks, utility providers). Hence forcing firms to set a price equal to marginal cost would lead to them making a loss. e.g. a price of P* above would not be viable, as it would lead to the loss represented by the shaded area. In the pist this has led to nationalisation of industries, as a private sector form would not be willing to operate at a loss and the governments did not want natural monopolies to act as profit-maximising monopolists and make supernormal profits.

In the UK, regulation focused on price has specified price increases each year below changes in the retail price index (RPI), knwon as the RPI – X rule. It was difficult for the government to set these, as the companies typically have more information about their costs than the government does (assymetric information). Also, this relies on a certain amount of X-inefficiencies being reduced by the firm, but over time these X-inefficiencies will be gradually squeezed out, which will allow little room for further productivity gains. Regulatory capture is also a worry, where the close relationship between a firm and their regulators can lead to the firm dictating the conditions.

Another alternative is instead of limiting price, to specify a limit on the company’s rate of return, however this can also be seen as disincentivising to a firm.

Task 1

Task 2

Find out which about the agencies that are responsible for competition policy in Georgia? How effective do you think they have been in promoting competition amongst firms in the economy.

Task 3

Task 4

Task 5

Task 6

Task 7