Initial Task

Quantity Theory of Money

Aggregate expenditure and the money supply both influence each other.

The quantity theory of money tries to explain this relationship using the Fisher equation: MV = PT, now more often written as MV = PY, where:

- M is the money supply;

- V is the velocity of circulation (i.e. the number of times money changes hands);

- P is the price level; and

- T or Y is the transactions or output of the economy.

Monetarists assume that V and Y are constant and not affected by changes in the money supply. Hence a change in the money supply causes an equal percentage change in the price level.

e.g. Suppose:

- Initial money supply is $80b;

- Velocity of circulation is 5;

- Price level is 100; and

- Output is 4b.

If V and Y remain unchanged, a 50% increase in the money supply to $120b would cause the price level to also rise 50% to 150.

Whilst Monetarists argue that inflation is a monetary phenomenon, Keynesians argue that as V and Y can change when the money supply changes, we cannot predict the impact that a change in M will have on P.

Broad and Narrow Money

The money supply refers to all money in the economy, including currency in circulation and bank deposits. Measuring money supply is complicated.

If something fulfils the functions of money, economists define it as money, however things may change over time in the extent to which they fulfil these functions.

The two main ways the government measures the money supply are:

- Narrow money – Notes in circulation, cash held in banks and balances held by commercial banks at the central bank. Also known as the monetary base;

- Broad money – All of the above items, plus a range of items concerned with money’s function as a store of value, e.g. funds held in a savings account.

Sources of the money supply

An increase in the money supply can be caused by:

- An increase in commercial bank lending;

- An increase in government spending financed by borrowing from commercial banks;

- An increase in government spending finance by borrowing from the central bank;

- Repurchase of previously sold government bonds; or

- More money entering than leaving the country.

Commercial banks

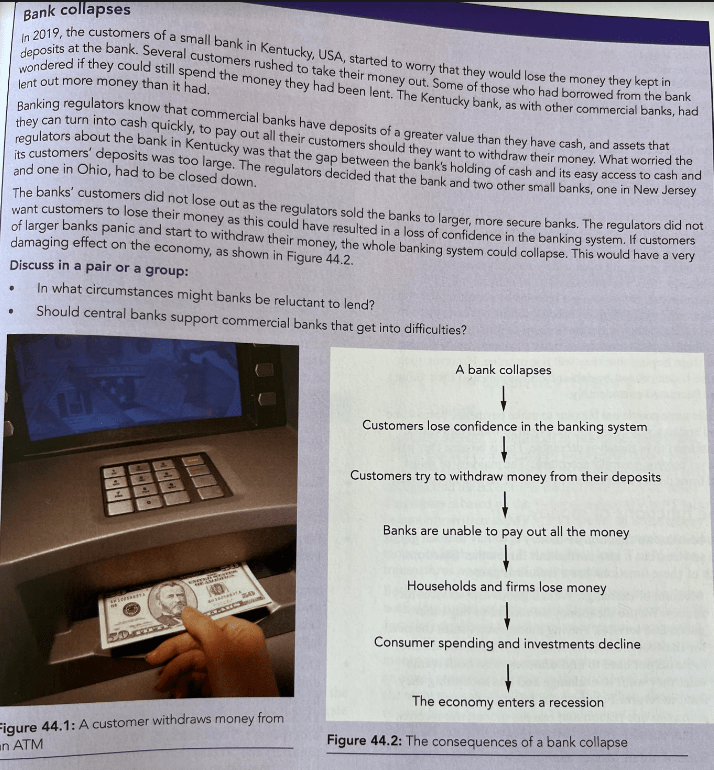

Commercial banks, also known as retail banks, make profit by lending money to customers. In doing so they create money. Historically, banks realised that at any given time only a small proportion of deposits held at a bank are turned into cash. People usually make payments electronically (e.g. with credit cards). Such payments require entries in the banks’ records and not payment of cash. Because of this, banks can create more deposits than they have liquid assets.

The lower a bank keeps its liquidity ratio (proportion of liquid assets to total liabilities), the more they can lend. However keeping this too low is risky, as it can mean they are unable to satisfy their customers’ demands for cash (part of the problem witnessed during the 2008 economic crisis).

In deciding what liquidity ratio to keep, a bank can also calculate its credit multiplier, which shows how much liquid asset is needed to enable a bank to increase its liabilities. This multiplier is calculated as “Value of new assets created” ÷ “Value of change in liquid assets”

e.g. If deposits rise by $600m as a result of a new cash deposit of $100m, the credit multiplier is 6. The credit multiplier can also be calculated as 100 ÷ “liquidity ratio”.

In reality, a bank may not lend as much as implied by its credit multiplier, due to a lack of demand from borrowers (that are considered by the bank to be credit worthy). Note that lending to borrowers with poor credit ratings is a high risk activity due to the risk of default (again as evidenced during the 2008 economic crisis).

A central bank may try to influence the activities of commercial banks. It can do this by engaging in open market operations (e.g. buying or selling government securities)

Task. Commercial Bank Customers

Task. Credit Multiplier and Liquidity Ratio

A bank has a liquidity ratio of 4%. It receives an additional cash deposit of $50,000. Calculate:

- The credit multiplier; and

- The potential increase in bank lending.

Government Spending

Government spending is funded by taxation and by borrowing. Borrowing can be by selling government securities (bonds), in which case it will be using existing money. Borrowing from commercial banks or the central bank will cause an increase in the money supply.

When the interest rate is very low, a central bank may use quantitative easing as a method to increase aggregate demand. This involves a central bank buying government bonds from financial institutions such as commercial banks in order to increase the money supply. As this helps commercial banks have more liquid assets, it is hoped to induce the commercial banks to lend more, thus increasing investment and consumer expenditure, and hence aggregate demand. This method was used by Japan in the 1990s and by the US, Europe and the UK during recent years.

Total currency flow on the balance of payments is the net outflow or inflow of money due to international transactions recorded in the current, capital and financial accounts. If the central bank keeps the exchange rate below equilibrium, there will be an inflow, i.e. an increase in the country’s money supply.

A change in monetary policy working through the economy by changing aggregate demand, price level and GDP is called the monetary transmission mechanism. It has several links – for instance an increase in money supply may lower the interest rate, which may then lead to increased aggregate demand, which may increase one or both of output and the price level.

Task – Government Securities

Keynesian and monetarist theoretical approaches

Keynesians believe that market forces cannot be relied upon to ensure a full employment level of GDP (avoidance of unemployment is a key priority for them). They support government intervention to influence the level of economic activity. For instance, if there is high unemployment, they believe that the government should use a deficit budget to increase aggregate demand.

Monetarists (e.g. Milton Friedman) consider controlling inflation to be a top priority for government. They consider inflation to be a result of excessive growth of the money supply. They consider that trying to reduce unemployment by increasing government spending will only lead to an increase in inflation in the long run. They see the economy as inherently stable unless disturbed by erratic changes in the growth of the money supply.

Liquidity Preference Theory

Keynesians suggest that the interest rate is determined by demand for and supply of money. They consider the supply of money to be determined by the central bank and fixed in the short run. They explain demand for money using liquidity preference, i.e three key motives for households and firms to hold wealth in money form:

- Transactions motive – The need for money to make everyday purchases and meet everyday payments. This is directly proportional to income received and inversely proportional to frequency of income payments;

- Precautionary motive – The need to hold money to meet unexpected expenses or take advantage of unanticipated bargains. These first two motives are sometimes called active balances as they are likely to be spent in the near future. They are relatively inelastic, as a rise in the interest rate will not lead to households and firms significantly reducing them;

- Speculative motive – By contrast, this is an interest elastic balance, sometimes called an idle balance, often held when the returns from holding financial assets are considered low.

Firms and households may hold government bonds (effectively loaning money to the government). The price and the interest rate of government bonds move in opposite directions. e.g. If government bond with a face value of $100 and a fixed interest rate of 5% increases in price to $200, the interest paid will then represent only 2.5% of the price of the bond. Households and firms will choose to hold money if the price of bonds is high and expected to fall, as they will not be sacrificing much interest and they will be afraid of capital loss.

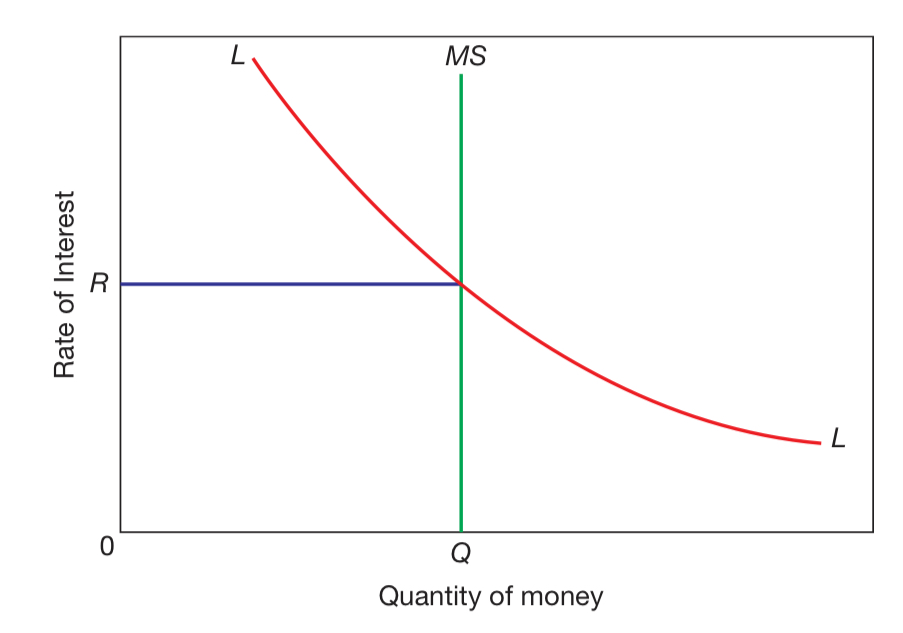

The diagram below shows the combined transactions, precautionary and speculative motives for holding money in the form of liquidity preference (or demand) for money. Interest rate is R, which is where the liquidity preference curve meets the supply of money curve.

As illustrated below, an increase in the money supply will cause a fall in the rate of interest. This is due to some households and firms having higher money balances than they prefer to hold and therefore using some to buy financial assets. A rise in demand for government assets causes an increase in the price of bonds and a decrease in the rate of interest.

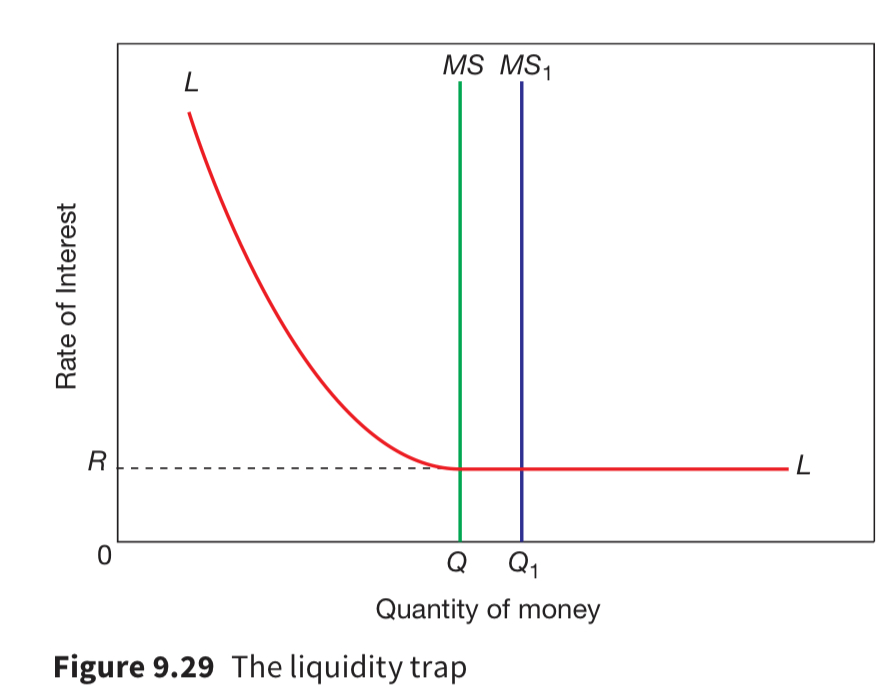

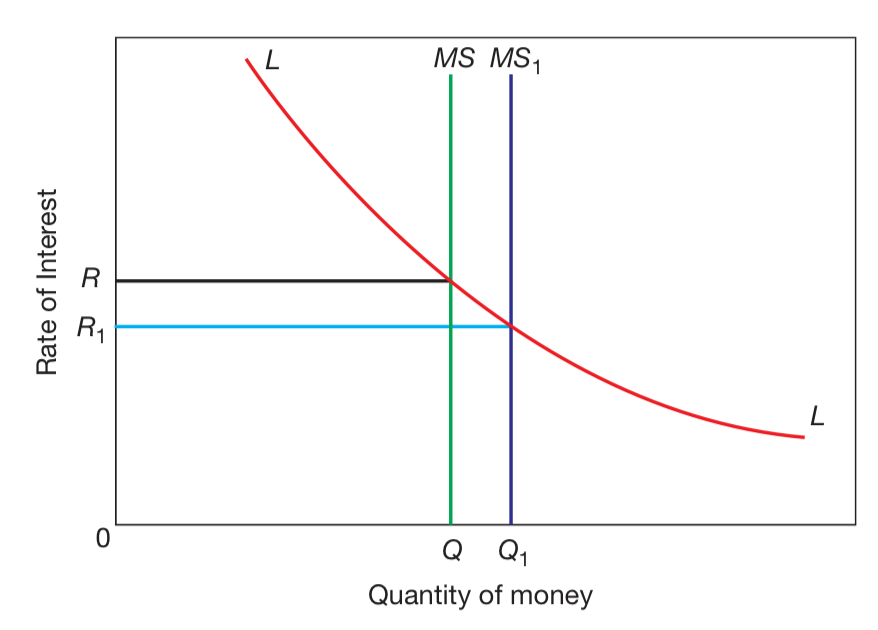

Liquidity Trap

Although Keynesians consider an increase in money supply to cause the rate of interest to fall, Keynes also describes a situation, the liquidity trap, when it would not be possible to drive down the interest rate by increasing the money supply. This could occur when the rate of interest is very low and the price of bonds is very high. Speculators would anticipate the price of bonds falling in the future and so if the money supply was increased they would hold the extra money. They wouldn’t buy bonds for fear of making a capital loss, and because the return from them would be low.

The below diagram shows that at interest rate R demand for money becomes perfectly elastic and increasing the money supply has no effect on the rate of interest: